Rent payments, often a household’s largest expense, have long been excluded from credit histories despite their clear predictive value. That is beginning to change as major credit scoring models, along with Fannie Mae, Freddie Mac, and fintech platforms, move to incorporate rental data.

The benefits of rent reporting for residents with no or thin credit profiles have been backed up by research. A recent Urban Institute study found that reporting on-time rent payments significantly boosted study participants’ credit scores. There are also numerous benefits for operators. RealPage reports that properties offering rent reporting experience a 20–25% increase in on-time payments. Residents are more likely to pay rent on time when they know that their payment history can impact their credit profile.

Rent reporting may not be widely practiced today, especially among smaller multifamily operators, but that is gradually changing. Operators who capitalize on rent reporting have a chance to be early adopters and seize on a trend that is beginning to reshape multifamily operations.

This Insights by Blueprint report examines the state of rent reporting and rewards in the multifamily market. The takeaways include:

- The main forces driving the adoption of rent reporting and rewards

- The tangible benefits for operators and residents

- The key vendors offering these services

- How operators can maximize ROI from these programs

- The future outlook for rent reporting and rewards

The case for rent reporting

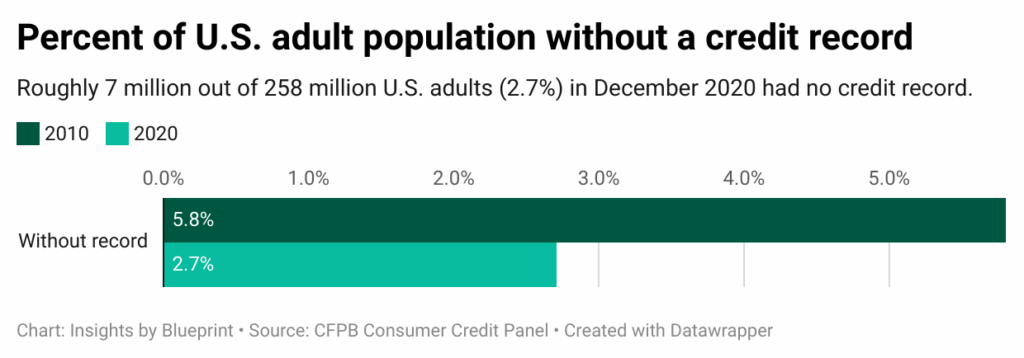

About seven million U.S. adults are considered “credit invisible,” according to a June 2025 update to Consumer Financial Protection Bureau data. “Credit invisible” refers to those who do not have a credit history with any of the three major credit bureaus (Equifax, Experian, and TransUnion).

Studies show that renters are disproportionately represented among those with credit invisibility compared to homeowners. Homeowners have mortgages, which are automatically reported and help build their credit history, while renters often lack similar tradelines. Many “credit-invisible” renters are younger adults, immigrants, or low-income renters who stand to gain the greatest benefit from building credit through rent reporting.

In the U.S. economy, it is exceedingly difficult to get by without access to the credit system. Consumers with higher scores typically qualify for a broader range of financial products at lower interest rates, and responsible use of those products further strengthens their credit profile. By contrast, individuals with limited or unfavorable credit histories often face restricted access, higher borrowing costs, and reduced housing opportunities, which can amount to thousands of dollars in annual costs.

Rental payment reporting aims to help change that. It is the practice of sending rental payment data, especially on-time payments, to the major credit bureaus so that it can be factored into a renter’s credit score.

How it works:

- Tradeline creation: When an operator or a third-party service reports rent, it creates a tradeline on the renter’s credit report, similar to a credit card or auto loan.

- Positive impact: Consistent, on-time payments help renters build or improve their credit scores, making it easier to qualify for mortgages, loans, and other financial products.

- Limited negative impact: Many programs report only positive payments (on-time rent), meaning missed payments aren’t automatically shared unless the account is sent to collections. This “positive-only” model reduces risk for renters.

- Implementation: Operators can opt in to provide this as a resident amenity, or tenants can sign up individually through certain apps and platforms.

Despite the recent push for rent reporting, less than 5% of rental history data is in the credit files, according to 2024 data from the Urban Institute, a Washington, D.C.-based think tank. Urban Institute research also reveals that 45% of consumers are unsure if their rent is reported, and many who say their rent is reported are “likely misinformed.”

Ethan Dornhelm, VP of Scores and Predictive Analytics at FICO, notes that as of 2024, roughly 2.7 million consumers have rental tradelines reported in their credit files, just 3.5% of the nation’s 77 million renters. Those with at least one rental tradeline tend to represent younger, credit-building populations, with an average age of 38 and an average FICO Score of 650. By contrast, the typical U.S. credit filer is 53 years old with a score of 715, underscoring both the relative youth and the steeper financial climb faced by renters who do manage to have their payments reported.

This massive gap highlights both the challenge and the scale of the opportunity for multifamily operators and rent reporting vendors. Rental payment reporting adoption today is skewed toward institutional portfolios of more than 1,000 units.

These owners and operators are early movers because they have the infrastructure, capital, and scale to integrate rent reporting and rewards across entire portfolios. Smaller operators, who manage the majority of the nation’s rental stock, remain largely underserved.

This dynamic sets the stage for a market inflection point. For large owners, rent reporting is emerging as a differentiator tied to collections, occupancy, and investor-facing ESG metrics. For smaller operators, barriers such as cost, system integration, and bandwidth remain real. Fintech vendors are developing solutions designed to bring these landlords into the fold.

Just as online rent payment portals shifted from rare to expected within a decade, rent reporting and rewards may be on a trajectory to become embedded in leases, loyalty structures, and resident benefit packages. The timing of that shift will depend on three factors: policy momentum at the state and federal levels, innovation from fintech platforms, and operators’ ability to prove the ROI in both resident outcomes and property performance.

What the data says about rent reporting

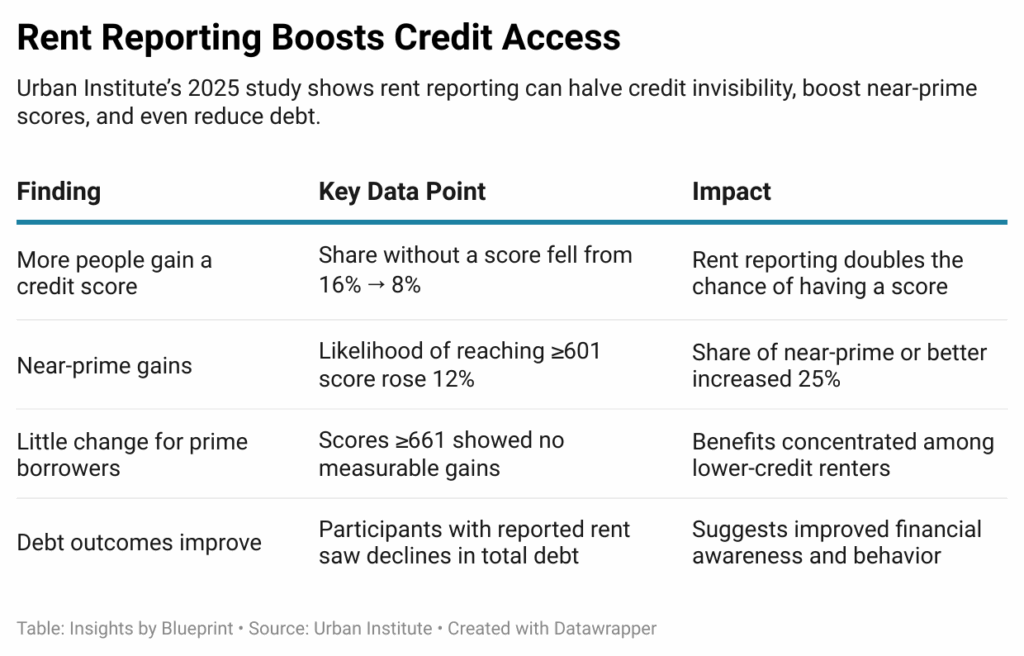

In June 2025, the Urban Institute released the first randomized study of rent reporting and its impact on credit scores. The research demonstrates that rent reporting can help individuals establish a credit score for the first time or improve their existing score.

The research revealed:

- Rent reporting increases the likelihood of having a credit score

- Using VantageScore, the study found that participants whose rent information was reported were significantly more likely to have sufficient data for a score.

- Among participants without a credit score at the outset, the share without a score was halved, from 16% to 8%.

- Significant gains were observed among those with weaker credit histories

- Rent reporting increased the likelihood of achieving at least a near-prime score (VantageScore ≥ 601) by 12%.

- For participants whose rents were reported, the share with near-prime or better scores rose by 25%.

- Limited effects for prime borrowers

- Study participants who already had a prime credit score of 661 or higher experienced no measurable gains in their score. For these people, the benefits of rent reporting likely don’t justify potential program fees.

- Study participants who already had a prime credit score of 661 or higher experienced no measurable gains in their score. For these people, the benefits of rent reporting likely don’t justify potential program fees.

- Unexpected improvements in debt outcomes

- Interestingly, the researchers found that participants whose rent payments were reported also saw declines in total debt compared to the control group.

- The researchers said the drop in total debt may be attributed to improved financial awareness, with participants recognizing the value of strong credit and being more proactive in managing debt.

The benefits for operators

Although rent reporting and rewards are usually promoted as benefits for residents, they also create advantages for property owners and managers. By encouraging consistent payment behavior, these programs can strengthen cash flow, reduce turnover, and generate data that supports more informed portfolio decisions.

- Improved collections. RealPage reports that properties offering rent reporting experience a 20–25% increase in on-time payments. When residents understand that their rent history can impact their credit profile, they are more likely to pay by the due date.

- Higher renewal rates. Programs that link rent reporting with rewards have been shown to increase resident loyalty. Stake reports renewal rates about 30% higher for residents enrolled in its cashback program.

- Predictive risk management. Esusu adds a new layer by aggregating portfolio-level credit score trends. Tracking shifts in resident credit profiles allows operators to forecast delinquency risk before it manifests in missed payments. If scores begin trending downward across a segment of units, owners can intervene with support services or payment plans, stabilizing NOI and avoiding costly turnover.

Many operators classify these programs alongside yield management tools or advanced property management integrations as investments designed to deliver measurable returns. Unlike concessions, which are short-term or one-off, rent reporting and rewards establish ongoing incentives that encourage resident behaviors aligned with ownership objectives.

Rewards programs: Perception vs. reality

Do rewards programs benefit residents that much? A strong argument can be made that the true benefit of these incentive programs tilts heavily in the operator’s favor.

For residents, the financial benefit of rewards programs is usually limited. Most platforms, such as Piñata, provide around $100 to $150 in value per year, often through cashback or points that can be redeemed for goods and services. That figure equates to approximately 0.6% of Moody’s average annual rent figure. A resident would have to stay in their unit at least nine years to get a value comparable to the average multifamily rent concession.

While rent rewards, such as cash back, may help with groceries, fuel, or a portion of childcare, they’re negligible when considered in relation to broader affordability challenges. In comparison, a common multifamily concession, such as “one month free,” can be worth thousands of dollars over the course of a lease. Fannie Mae’s January 2025 multifamily market commentary reports that while concession rates have been increasing recently, they generally remain below one month’s free rent, or roughly 8.3% of annual rent.

From the operator’s perspective, rewards programs create a far more favorable equation:

- Lower-cost alternative to concessions. Providers like Incentco position their points-based systems as an operationally efficient substitute for blanket rent discounts. With each point valued at just a few cents, rewards cost a fraction of concessions while still generating a stronger perception of ongoing value.

- Perceived value > absolute value. The “psychology of points” plays a critical role. While $10 in cash back may not significantly impact affordability, residents may view rewards as a sign that their loyalty is recognized. This sense of being valued, especially when tied to on-time payments, creates stickiness and reduces turnover risk without requiring operators to give up meaningful rent revenue.

- Retention, not relief. Rewards foster a cycle of positive reinforcement. Residents who accumulate points or perks tied to their rental behavior may be more likely to renew to avoid losing the benefits they have accumulated.

Critics note that the value of renter rewards is often overstated. A single 10% rent increase can wipe out the benefits of such programs for many years to come. For this reason, rewards are better positioned as tools for engagement and retention rather than as solutions to housing affordability. Framing them otherwise may weaken resident trust.

The ESG case for rent reporting

Institutional investors are placing greater emphasis on measurable social outcomes, the “S” component of ESG frameworks. Investors and lenders are seeking data that can show precise results. Rent reporting is positioned to provide that evidence. By turning a routine operational practice into trackable indicators of financial inclusion, owners can report on outcomes such as:

- New credit scores created. Each renter who moves from “credit invisible” to having a tradeline is a tangible marker of impact. In Esusu’s case, over 250,000 renters have established new credit scores since adoption, offering portfolio owners hard numbers to showcase.

- Average credit score gains. Reporting on portfolio-wide improvements—e.g., a 45-point average credit score increase among participants—not only highlights resident progress but also links directly to risk reduction from an operator’s perspective.

- Participation rates as ESG KPIs. A helpful indicator is the share of households that sign up when given the option. This provides an easy way to show engagement and inclusion.

The vendor landscape

As rent reporting and rewards move from early adoption to broader consideration, the vendor ecosystem is evolving quickly. Each platform brings a distinct focus, with some built around inclusion and compliance, while others focus more on engagement and rewards. For multifamily operators, understanding these differences is important for picking the right partner.

Esusu

Esusu, founded in 2018, is recognized as one of the pioneers in rent reporting. The platform connects with the three major credit bureaus and integrates with top property management systems, including Yardi, RealPage, MRI, and Entrata. Compliance is a core focus. Esusu adheres to FCRA standards and uses encrypted, cloud-based systems to securely manage rental payment data. Each month, resident payment information is sent to the bureaus through certified APIs. On the operator side, owners and managers log into a secure dashboard to submit reports, monitor results, and track performance.

Beyond reporting, Esusu offers a range of financial wellness tools. These include credit monitoring, financial education, and one-on-one coaching for residents. The company offers interest-free rent relief loans aimed at preventing evictions. Residents access a mobile app to track credit progress and explore resources. Operators gain access to dashboards that highlight social impact metrics. These features can be folded into ESG reporting and investor updates.

Esusu generally works best with portfolios of 100 units or more, though it can support a wide variety of housing providers. Integration is straightforward for operators already on major property management platforms, and the system can be adapted for other providers as well.

The company’s pricing model includes a one-time setup fee of $3,500 and an ongoing monthly fee of approximately $2 per unit. Discounts are available for larger portfolios. Pricing is flexible and based on portfolio size and service scope.

Blueprint recommendation: Esusu provides a strong mix of regulatory compliance, resident benefits, and transparency for investors. Its simple integration with PMS platforms reduces operational hurdles, while its FCRA-compliant reporting framework reduces regulatory and reputational risk.

RentPlus

Entrata expanded its platform in 2023 by acquiring Rent Dynamics, which included the RentPlus program as part of its resident-facing services. RentPlus differentiates itself in the rent reporting market with a feature that allows up to 24 months of past on-time rental payments to be reported. That gives residents a meaningful head start in establishing or improving their credit.

This capability has produced strong results. Average engagement with the platform exceeds 80%, while residents experience a 48-point credit score increase within their first year of enrollment. RentPlus is especially beneficial for operators already using Entrata’s management system, as it integrates seamlessly into existing workflows. The platform is generally designed for housing operators managing at least 500 units.

Pricing depends on property type:

- Conventional properties: $9.95 per resident each month, with a $3 revenue share.

- Affordable properties: $6.95 per resident each month, with opportunities for reduced pricing if landlords choose to subsidize the cost.

Blueprint recommendation: RentPlus is a strong option for larger operators seeking a high-engagement program that supports residents’ credit growth. For operators already on Entrata’s platform, it’s a no-brainer that combines resident financial inclusion benefits with positive, measurable returns.

Jetty Credit

Jetty is a comprehensive platform that simplifies the rental experience for residents and property owners. Its rent reporting model is “positive-only,” so it only records on-time payments. This approach gives credit-invisible renters an opportunity to build credit without adversely impacting those who may already be financially vulnerable.

As an approved vendor in Fannie Mae’s Positive Rent Payment pilot, Jetty appeals to mission-driven owners seeking scalable ways to demonstrate measurable social impact. With built-in PMS integrations and a straightforward enrollment process, the system is easily adopted by operators.

The platform goes well beyond rent reporting with a suite of resident financial tools:

- Jetty Deposit – A security deposit alternative that lowers up-front move-in costs while still protecting owners.

- Jetty Rent – A flexible rent payment program that helps residents manage cash flow.

- Jetty Protect – Renters’ insurance covering personal belongings and liability, with customizable options.

Pricing:

- Jetty Deposit: Starts at $7 per month, with pricing determined by coverage level and credit profile.

- Jetty Credit (rent reporting): Free for properties financed by Fannie Mae or Freddie Mac, with subscription options for other renters.

- Jetty Protect: Insurance plans start at $5 per month, with flexible coverage choices.

Blueprint recommendation: Jetty has positioned itself as a resident-friendly platform that combines credit-building with financial protection. Jetty is especially useful for owners focused on ESG and affordable housing, and it’s a low-friction platform that can enhance both resident financial stability and portfolio performance.

Self Rent Reporting

Self Financial acquired LevelCredit in 2022, which is the parent company of RentTrack. The move expanded Self Financial’s suite of credit-building tools, and the platform has since been rebranded as Self Rent Reporting. Unlike many other platforms, Self Rent Reporting allows renters to enroll directly without the involvement of operators or property managers. This makes the service of the more flexible rent reporting solutions on the market.

Self Rent Reporting is designed to increase credit visibility by reporting positive payment history to all three major credit bureaus. Key features include:

- Monthly Rent Reporting: Automatic verification and reporting of rent payments. Late or missed payments are not reported, protecting renters from adverse impacts.

- Bills Reporting: Adds positive payment history for utilities and telecom bills, such as cell phone, water, gas, and electric, to TransUnion credit files.

- LookBack Reporting: Retroactive reporting of up to 24 months of past rent and utility payments with current providers, enabling users to quickly build a longer credit history.

- Credit Monitoring: Alerts users to suspicious activity on their TransUnion credit file.

- Identity Theft Insurance: Includes $1 million in zero-deductible protection for subscribers.

Pricing:

- Basic Plan: Free tri-bureau rent reporting.

- Upgraded Plan: $6.95 per month, which adds utility/telecom bill reporting, TransUnion credit monitoring, and identity theft insurance.

- Retroactive Reporting: One-time fee of $49.95 for up to 24 months of backdated rent and utility payments, available with both free and paid plans.

Blueprint recommendation: Self Rent Reporting takes a unique angle by positioning itself as a widely accessible, resident-first solution that offers rent reporting without property management involvement. It’s an attractive option for operators, especially smaller ones, to encourage residents to use, and it doesn’t require new system integrations.

Bilt

On the rewards side, Bilt has quickly established itself as one of the most popular and innovative loyalty platforms in rental housing. Its program is structured around aspirational goals and enables residents to earn and redeem points for travel as well as future housing goals like rent credits and home down payments. Bilt’s incentive program tends to resonate the best with young, urban renters who seek lifestyle experiences and long-term financial health.

Renters earn Bilt Points on rent payments, which can be redeemed in several ways:

- Travel: Transfers to 16 airline partners and five hotel programs, positioning Bilt among the most valuable transferable points currencies. Points are worth at least 1.25–1.5¢ each when redeemed through Bilt’s travel portal or transfer network.

- Housing: Points may be applied toward future rent or converted into down payment contributions with select mortgage lenders at a rate of 1.5¢ per point.

- Everyday Value: While earning points can take time, they carry outsized upside for experienced award travelers and provide an accessible entry point for renters new to points and miles.

Renters in Bilt Alliance properties can pay directly through the Bilt app, while non-partner renters can have Bilt mail a check to their landlord or use a virtual account and routing number, ensuring broad accessibility.

Blueprint recommendation: Bilt is often cited as one of the better loyalty and financial empowerment programs available to multifamily owners, especially those with Class A or lifestyle-focused communities. Bilt Rewards can offer a unique resident amenity that can function as both a marketing and retention tool in competitive rental markets.

Stake

Stake is a rent rewards program that takes a different approach than Bilt. Rather than offering points or gift cards, Stake focused on cash-back incentives that encourage residents to pay on time while also helping operators improve their cash flow. Stake is designed to offer immediate value by depositing money directly into renters’ accounts.

Residents earn cash back on rent payments, with opportunities to unlock higher returns:

- An additional 2% bonus for keeping at least 80% of funds in a Stake account.

- 1% back on everyday purchases through Stake’s ecosystem.

- Bonus rewards include $15 for linking a bank account (with support for over 11,000 banks and Venmo).

In addition, renters receive fee reimbursements and access to a complimentary concierge service that can assist with household needs, such as hanging art, pet sitting, or housekeeping.

Stake generates revenue by charging owners and operators a $49 monthly subscription fee to deploy the program across their portfolio. Participation is free for renters, which removes barriers to adoption and supports stronger engagement.

Blueprint recommendation: Stake appeals to residents who prioritize immediate financial benefits, which could go toward everyday expenses like groceries, fuel, or childcare. For owners, the platform is a low-cost, potentially high-impact tool that can improve retention and collections.

Piñata

Rounding out our recommendations for rent rewards programs is Piñata, a platform that also offers credit reporting services. Renters earn Piñata points for paying rent on time, which can then be redeemed for gift cards and special offers for major retailers, such as Starbucks, Target, Best Buy, and Amazon. Piñata sweetens the pot with extras like raffles, bonus perks, and a points marketplace, which keeps engagement on the platform higher.

The company’s reach has recently grown via a partnership with MRI Software, which has integrated Piñata into the MRI RentPayment system. This enables residents to access rewards, credit-building benefits, and the points marketplace from the same portal they already use to pay rent, thereby creating a more seamless process for operators and renters.

Blueprint recommendation: By combining credit reporting with tangible financial incentives, Piñata offers clear benefits to both residents and property managers. Its partnership with MRI strengthens the platform as a scalable, resident-focused solution that makes rent payment both a financial tool and a source of everyday value.

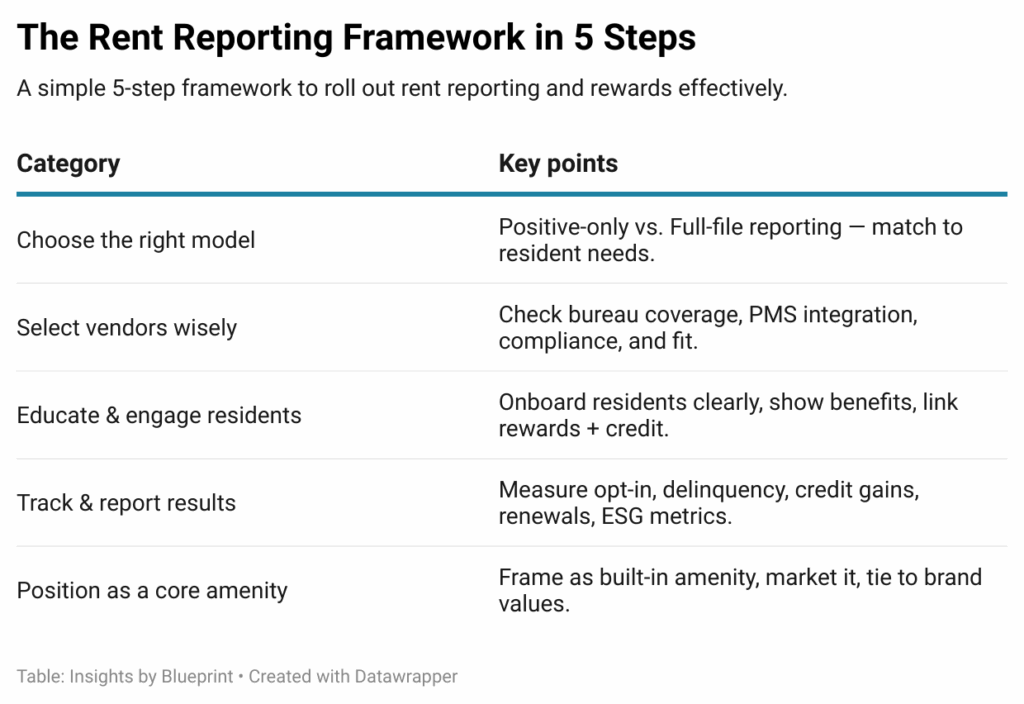

The rent reporting framework in 5 steps

Rolling out rent reporting and rewards requires thoughtful alignment of model, vendor, resident engagement, and measurement. The following playbook distills best practices from early adopters and vendor case studies into a clear framework for owners and operators.

Choose the right model

- Positive-only rent reporting. This model is often utilized in affordable housing or ESG-focused portfolios. Only on-time payments are reported, shielding residents from negative credit marks. The result is stronger inclusion outcomes that fit well with impact reporting frameworks.

- Full-file rent reporting. This version records both on-time and late payments. It is more common in market-rate or Class A housing, where residents are generally more financially stable. The model can lead to bigger improvements in payment behavior, but it also requires clear communication to avoid resident concerns.

Key question: Does your resident base need protection and inclusion (positive-only) or incentive and discipline (full-file)?

Select vendors wisely

- Credit bureau coverage: Ensure the provider reports to all three major credit bureaus for maximum impact on the resident’s credit.

- PMS integration: Look for vendors that integrate seamlessly with Yardi, RealPage, Entrata, AppFolio, or MRI. Poor integration adds administrative friction and increases the risk of errors.

- Data security & compliance: Prioritize vendors with SOC 2 certification, FCRA-compliant data furnishing, and clear dispute resolution processes. Liability for errors can be significant, and compliance failures can erode resident trust.

- Differentiators: Match vendor strengths to portfolio needs. Esusu for ESG analytics, Entrata for retroactive reporting, Jetty for positive-only reporting, Bilt or Stake for rewards.

Key question: Which vendor aligns best with your compliance risk tolerance and resident profile?

Educate & engage residents

- Onboarding method matters. In-person or live virtual onboarding drives higher opt-in rates than email campaigns alone. Property managers should be trained to present the program clearly during leasing and renewal conversations.

- Make it tangible. Share examples of average credit score improvements (e.g., “Our residents typically see a 40-point boost within six months”) and show how that translates into real benefits (lower car loan rates, credit card approvals).

- Connect short-term and long-term. Combine credit education with rewards, so residents receive immediate value, such as cash back, while also learning how on-time payments build credit for the future.

Key question: How are abstract benefits being turned into outcomes that residents can clearly recognize and experience?

Track & report results

Track both resident outcomes and operational impact to show ROI:

- Opt-in rate: Share of eligible residents who choose to enroll.

- Delinquency rate change: Difference in late-payment rates before and after the program.

- Credit score gains: Average improvement among participating residents.

- Renewal lift: Gap in renewal rates between participants and non-participants.

- ESG Metrics: New credit scores created, participation percentages, and average credit score lift.

This data validates performance internally and supports investor reporting and ESG disclosures.

Position as a core amenity

- Amenity, not add-on. Frame rent reporting like Wi-Fi, gyms, or package lockers: a built-in part of the living experience, not an optional upcharge. Mandatory renter-paid fees risk “junk fee” backlash.

- Integrate into marketing. Highlight credit building and rewards in leasing tours, digital listings, and investor decks. Resident success stories make the impact relatable and persuasive.

- Tie to brand values. Whether your community emphasizes financial empowerment, premium lifestyle, or ESG leadership, position rent reporting as an extension of that identity.

The junk fee debate

Rent reporting has clear credit-building benefits for residents, but cost structures vary from one vendor to another. Residents may have to pay subscription or enrollment fees directly in some cases. In other cases, the costs are absorbed by operators or through public subsidies.

Charging fees to residents for rent reporting has drawn criticism because it risks being perceived as a charge with little immediate value. “If you’re just talking about credit reporting that has longer-term benefits, that may feel like a junk fee,” says Rowland Hobbs, CEO of Stake.

To avoid that “junk fee” perception, Hobbs believes operators and vendors must frame their programs as more than just simple credit reporting. Combining credit reporting with immediate rewards may create a more balanced approach. Operators also benefit when the programs produce measurable results, such as reliable data on collections, renewals, and resident satisfaction. That helps them measure ROI more effectively.

Hobbs also explains that while rent reporting can have a significant positive impact on credit scores, some renters may lack the financial literacy to understand its importance. “They may also be a first-generation American and not understand our credit system,” he says.

This is why most vendors encourage operators to opt in residents automatically for rent reporting programs, a practice that Fannie Mae and Freddie Mac have also endorsed. If residents must opt into it, that assumes they understand credit. An opt-in strategy means residents who need it the most may be left behind.

Because the long-term benefits of credit building aren’t always obvious to residents, many providers have introduced hybrid models. These combine rent reporting with short-term perks, such as cash-back rewards, so renters receive something they can use right away while still building credit for the future.

The trend is similar to how credit cards evolved, where rewards became an expected feature rather than an extra perk. Programs that do not deliver clear, near-term value may risk lower adoption and dissatisfaction among residents.

The next phase of rent reporting & rewards

The renter rewards and reporting market is entering a new phase of experimentation, new regulations, and industry consolidation. Operators are currently dealing with a patchwork of platforms, some centered on credit reporting, others on rewards programs, and still others on a broader array of financial wellness tools. This variety has spurred innovation but has also added layers of operational complexity.

By contrast, residents increasingly prefer unified and simplified solutions: platforms that combine payments, credit reporting, rewards, and financial wellness tools under a single umbrella. Competition among fintech providers is expected to accelerate consolidation, with success hinging on three factors: integration with property management systems, measurable resident and operational impact, and demonstrable ROI at scale.

Public policy is also adding momentum for rent reporting. As of April 2025, in California, AB 2747 requires landlords to offer residents the option to have their on-time rent payments reported to credit bureaus, effectively making it the first state to enshrine this practice in law. As of July 2025, the FHFA has mandated the use of VantageScore 4.0, which includes rental payment data, in underwriting for mortgages sold to Fannie Mae and Freddie Mac.

Below, we review three other key trends in multifamily rent reporting and rewards:

The open-platform model

Esusu has adopted an open-platform approach. Rewards are available but treated as one component of a broader ecosystem. “We have a third-party vendor that does rewards that people can sign up for and be on their platform,” explained co-founder Wemimo Abbey.

Instead of creating a closed ecosystem, Esusu works with partners and positions itself as a central hub for resident financial health. Abbey has likened the approach to Apple’s app store: residents can access rental insurance, other types of coverage, or even open a bank account, all within the platform. While rewards are included, Esusu’s core strength is in collecting rental data and connecting it to financial services that support long-term housing stability.

Rethinking rewards

Industry leaders are also raising concerns about the sustainability of point-based rewards. “You’re going to have this thing that naturally happens where everybody runs wild inflation on points because they just issue more points,” said Rowland Hobbs, CEO of Stake. The result, he warns, is declining value: “Points are going to become worth a lot less, and residents are going to feel like it’s the DMV giving them points.”

As a result, rewards may evolve into broader loyalty strategies. Hobb’s analogy to airlines is instructive: “When you fly on American versus Delta, you can see how they’re using their loyalty to move their business strategy.” In multifamily housing, loyalty programs are shifting from simple perks to core elements of retention, ancillary sales, and revenue growth.

Integration frustrations

A key obstacle to scaling these models lies in integration with property management systems (PMS). Platforms often work with major providers such as Yardi, Entrada, and RealPage, but experiences vary. “Some are better than others in terms of being startup- or vendor-friendly. Some are really difficult to work with. Some have really high tolls that you have to pay,” Hobbs of Stake explains.

Unlike the banking sector, which has adopted open frameworks to encourage innovation, the real estate sector has remained largely closed. PMS systems are often treated as profit centers, which can slow the adoption of outside tools. “It means the innovation moves more slowly because it’s harder for somebody to come in with a great idea,” Hobbs says. “To do that across ten different property management software, it’s going to be really expensive. So you’ve got to pick your one or two to start with.”

To address these barriers, some vendors are building robust API connections designed to plug into broader data ecosystems. “More and more properties are saying: this is our property management software, but we also have a bigger data lake we’re plugging into. We want to be able to run on top of that,” Hobbs says. Over the past five years, operators have become increasingly sophisticated in managing data, creating new opportunities for third-party platforms, even in traditionally closed environments.

Final takeaways

Rent reporting and rewards may soon move from niche perks into an expectation in the multifamily industry. For renters, the upside is clear: paying on time can help them build credit and put them on the path to better financial stability. Operators benefit from improved collections, higher renewal rates, and stronger ESG performance.

The trick is in how these programs are positioned. When residents view standard amenities as essential rather than bolt-on extras, they are more likely to embrace them. Choosing the right partner is also crucial, particularly one that strikes a balance between meaningful resident benefits and ROI for the property.

As with online rent payments, adoption may become much more widespread in rental housing sooner than many think. Wemimo Abbey, Co-Founder of Esusu, predicts that rent reporting will become standard multifamily practice within the next two to three years. Early movers will be best positioned to capture both resident loyalty and investor confidence.

– Nick Pipitone