Today’s report is from Joe Aamidor, founder of Aamidor Consulting, a product and market strategy consulting firm in smart buildings, working with vendors, investors and real estate leaders seeking to procure solutions. Joe also publishes Smart Building Insight, a bi-weekly market wrap up of smart buildings news. Find Joe on Linkedin or Substack, and please reach out if you want to speak about our work.

As software “eats the world” and real estate technology continues to advance, it is hard to keep pace with the state of innovation. Most real estate owners and operators have an expanding array of responsibilities and limited resources to complete them. Smart building technology is one category that is rapidly innovating, but may not yet be a priority of some real estate leaders.

We’ve observed that for most owners and operators, smart building tech remains somewhere between “interesting” and “we’ll get to it eventually.” That’s a problem, because the forces driving adoption such as rising energy costs, tightening sustainability mandates, labor shortages in facility management aren’t waiting. On the vendor landscape side, the challenge isn’t a lack of options. It’s the opposite. The market is fragmented across dozens of vendors, multiple product categories, and overlapping use cases. In fact, as we’ve covered in our Smart Building Insight newsletter, nearly every stage of the value chain is fragmented. An energy management platform might do some of what a sustainability reporting or fault detection tool does. A digital twin vendor might pitch analytics capabilities that sound a lot like automated system optimization. Without a clear framework, it’s easy to get lost in vendor demos and conference pitches without ever making a decision.

In this report, we break down the major categories of smart building technology, what they cost, and what kind of savings they can realistically deliver. Then we walk through a practical procurement approach — from baselining your current tech stack to defining use cases to evaluating vendors — so smart technology buyers can move from “interested” to “implemented.”

Overview of smart building tech

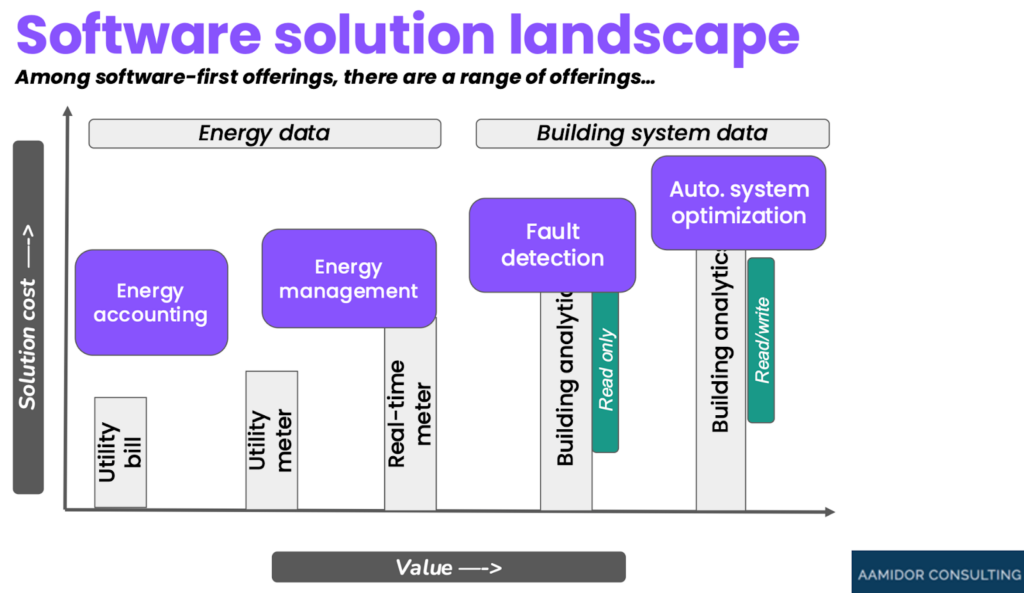

There are a number of ways to categorize smart building technology. But, the two best methods are by type of building, and type of application (which itself is based on the complexity and category of data collected, and how it is analyzed).

Different building types have a range of systems, from a utility energy meter to robust submetering, in addition to complexity of building controls (from a thermostat to a robust building automation system). These systems provide data for a smart building platform, but also may provide some capabilities that could otherwise be included in a smart building solution. There may be some duplication between the capabilities in the standard controls in the building and the supervisory smart building solution, with pros and cons of each.

If we focus on larger, more complex buildings – hundreds of thousands of feet, hundreds or more occupants, and typically used as an office, educational space, or other institutional purpose (such as a hospital), we have a few logical categories of smart building technology:

- Energy management: This can range from a basic utility bill aggregation platform to a more analytical offering that utilizes 15-minute interval data (usually real time, or near real time), to identify anomalies, support benchmarking between sites, and provides more proactive visibility than a utility bill arriving a few weeks after the billing period.

- Analytics. A bit of a catch-all, but typically focusing on more gradual data from some base building systems, such as the building automation system, to identify specific equipment issues or even flag maintenance issues before they would otherwise be observed. Fault detection and diagnostics is the most well-known type of application in this category.

- Automated system optimization. Moving beyond simply analyzing and flagging issues, there are some platforms that provide supervisory control over existing systems, which can drive savings and avoid maintenance issues without requiring a human to be in the loop. For buildings that are at risk of receiving a significant energy demand charge, such technologies could pre-cool a space, or let temperatures drift slightly – without requiring a building operator to get involved – to reduce those demand peaks. There are a range of other common applications for this technology, but in general, it delivers value without requiring a human to be all that involved.

- Digital twin. This category was initially defined as a different way to visualize data and model scenarios (e.g., what if employees don’t come into the office tomorrow), but now it tends to provide similar use cases as the categories above, though sometimes using a more BIM-style mapping interface to show all the data collected. We are including this category because it has some promise and should at least be on your radar if you are looking to procure technology in this industry.

There also are a large number of types of firms that offer these solutions, from OEMs which have built out cloud-based technology layers that fit naturally with their strong experience in equipment, base building systems, and also lifecycle services, to innovative startups which offering similar kinds of technology, but as an agnostic vendor seeking to integrate with any and all previously deployed systems. Moreover, there are facility management service providers, local and regional integrators and installers, and also adjacent firms, such as energy services firms, which sell energy reduction guarantees with no capital required upfront. All of these firms, and more, may offer smart building technology. These solutions could be built in house, or delivered via a partner.

While over simplified, this chart highlights the key categories of solution, general pricing benchmarks, and estimated savings. Note that the savings per building typically varies significantly, and achieved savings in a particular building will typically “average down” when the solution is deployed across a wider portfolio. This is usually a factor of some buildings being run well, and others being a long time from an audit or other proactive maintenance.

| Product Category | Avg Price ($/sq ft/yr)(Annual license) | Savings Opportunity | Notes |

| Utility bill /meter analysis | $0.01 | Under 5% | Energy accounting solution |

| Energy management (or, energy information system) | $0.02-$0.05 | 5-10% | Uses a real time energy meter. Portfolio-focused, delivers visibility, some anomaly detection and sustainability data compliance. |

| Fault detection and diagnostics (FDD) | $0.05-$0.10 | 5-15% | Pricing varies. Targets larger, complex buildings (with BAS) |

| Automated system optimization | $0.15-$0.25 | Up to 30% (but varies greatly) | Usually target larger, complex buildings (with chillers) |

Why smart building tech matters

While it may be under the radar, smart building technologies are emerging in importance to owners and operators who want to operate and deliver the best buildings and best space. As amenity-rich buildings focus on more than just great physical features – food and beverage, health clubs, etc – they should consider the operational technology layer, which includes smart building technologies.

Moreover, there are a number of key trends that are driving demand for smart building technology, such as:

- Demand for more amenitized space. Physical amenities are no longer enough, as tenants expect a personalized digital layer that can help them access their offices, find flexible spaces in a pinch, and even monitor and control comfort, indoor air quality, and lighting (daylight vs artificial light). Providing these amenities requires an interface to the base building systems – a core part of smart building technology.

- Labor shortage. Many facility engineering progressionals are retiring, and with their departures are also significant losses in knowledge of building operations. Moreover, to attract new employees to replace these team members, more advanced and modern technology is required. Smart building technology can help with both.

- Flexibility to hire best-of-breed service providers. This may not rise to the attention of senior real estate leaders, but related to the labor shortage are legacy service provider relationships for base building systems (fire/life safety, access control, HVAC, lighting, etc). In many cases the systems installed drive restrictions on which firms can be called for ongoing service. This strong product/system and service provider relationship can be detrimental to the building’s operation; some smart building technology platforms unlock these data streams.

- Increased energy costs. Energy costs are going up, and with their rise, there is more demand for energy efficiency. Energy costs are no longer predictable and manageable. Smart building technologies can help to identify waste and automate optimization of some systems to deliver greater savings (energy, operational and staff efficiency).

- Sustainability and decarbonization. Similar to the energy efficiency point, there also is an increasing need to benchmark and track building performance such as energy / carbon emissions. This can be driven by local laws or investors and other stakeholders.

How to procure smart building technology

So, how do leading organizations procure these technologies? We have a few recommendations based on work helping some firms procure these technologies and years of experience providing commercial due diligence on behalf of investors or to help vendors with competitive benchmarking and product strategy.

We recommend buyers of these solutions begin with a three step approach:

- Baseline current technology stack

Let’s start with an example: if a given building automation system is scheduled to be replaced in the coming years, a solution that integrates seamlessly with that BAS may not be that compelling over the long term. But, if you aren’t aware of this plan or even the presence of this vendor’s product, it’s unlikely that you will be well-positioned to acquire software to complement it.

So, as a first step, it is important to first understand the technology being used across your organization’s buildings – and who is using those solutions. This baselining exercise includes building automation systems (vendors and vintages), other base building control systems (e.g., security/access, lighting, other), and any cloud-based energy management or sustainability solutions. And, there may be more – but understanding what is currently being used will help identify gaps and drive solid future procurement decisions. Lastly, service contracts with firms with oversight of these systems, in addition to capital plans, also could be considered.

2. Run a wide process that narrows, not a narrow process that stalls.

Given that building portfolios have a wide array of systems and vendor relationships, there also are plenty of stakeholders. While it can be difficult to get all of these teams on the same page, we’ve observed that taking a narrow approach may cause procurement to stall. There is a sweet spot: understand the state of relevant systems in your portfolio (number 1, above), AND also be aware of the stakeholders using those systems. Communicate with them, take their feedback, and when relevant, include them in assessment and buying decisions.

There are many solutions in the wide smart buildings category overlap – a facility management offering likely has overlap with energy management, which has overlap with sustainability data management. There may be good reasons to buy individual solutions for each, but there should be some discussion of this approach (it shouldn’t just happen organically due to a logistical or communication issue). More tactically, there is a difference between buyers and users; both are important but play different roles. For example, tenant occupied buildings might have individual occupiers who use some of these capabilities (e.g., tenant billing), but they are not going to be involved directly in purchasing.

3. Identify key use cases or problems to solve

Smart building solutions deliver a multitude of solutions, but not all offerings do everything. And, not all building owners need offerings that “do everything”. There are a range of drivers that you may want to achieve, and all will be important to your portfolio. Mapping procurement decisions to one (or a few) key use cases will help to find the most compelling offerings (that actually solve those problems). It is more important to define what you want from these solutions than to let vendors wow you with their offerings. Lastly, some use cases are related: while sustainability mandates may be declining in focus, energy costs are rising, and some smart building technologies will address both of these issues.

Building on the last point above, we’ve observed a tendency to scout the market by seeing what is available – this can be driven by conference attendance or just sitting in on virtual webinars and other marketing activities. While all this has a place, it isn’t the first step in the procurement journey. In fact, it is far more important to spend time internally both identifying all the key stakeholders, but also understanding the current solutions used, gaps in those offerings, and the value proposition of investing in new technologies. For example, a firm may see rising energy costs as a financial risk, but also may recognize that the organization has very poor visibility into how it uses energy (especially at the portfolio level). This problem statement could be refined and detailed even further – and this serves as a strong set of requirements in which to go find vendors that can help.

And, given the fragmentation in the market – dozens or more vendors – it is important to define your needs carefully and early, as this will help to focus your vendor research efforts by promptly reducing the universe of viable vendors. In fact, the entire value chain is fragmented, as we analyzed in our newsletter, Smart Building Insight.

We have some other tactical tips to buyers:

- Standard pricing. Define a framework for vendors to present pricing, and use it to do a like-for-like comparison across all firms.

- Implementation matters too. Make sure to focus not only on product features, but deployment and implementation capabilities (and historical performance). We find that many vendors underestimate the costs and timelines for implementation, which can be detrimental to the buyers. And, this is a big effort for building owners and operators, so it’s good practice to ask each vendor what they need from you during implementation.

- Gather feedback from real customers. When you have a shortlist of vendors, request feedback or an opportunity to speak to each firm’s existing customers and ask about their experiences. In addition, review case studies to see real world results. It’s common for buyers to seek out references from clients in similar industries, but we think it also is important to review case studies and examples from clients that had the same problems. For example: an educational institution seeking to address comfort issues more proactively could find reference clients that also are universities, but it should also see if hospitals, lab space or other complex building clients had similar problems and resolution with a particular vendor.

- Product vs service. Given the fragmentation in the market, you may find that some firms have a product that has been built for a few of that vendor’s clients (and may or may not work for you). But, at the same time, it is possible that the vendor has a flexible kit of features that can be configured for each individual client. We have seen pros and cons for each approach – and simply recommend that any buyer at least is aware of both models. Some products work very well for a given client, but that user may have different specific goals and needs as your organization.

- Vendor churn is low. Based on our 15+ years of experience in this industry, we tend to see that vendor churn is very low. That means that most buyers stick with their vendors for years. For buyers, regardless of how long you expect to use a given product, it is likely that you will use it for a longer period of time.

Smart building technology is compelling and ready for deployment across buildings of all sizes and complexities. But, the fragmentation in the market, in addition to different applications and support for different use cases means that procurement processes must be diligent and goal-oriented. These recommendations should help you get started.

-Joe Aamidor

Find Joe on Linkedin or Substack, and please reach out if you want to speak about our work.