While mass timber has generated considerable excitement, it remains a relatively small slice of the real estate development market. As of June 2025, there were 2,524 multifamily, commercial, and institutional mass timber projects either built or underway in the U.S., according to Woodworks, a nonprofit that provides support to advance the use of wood in commercial construction. Growth has been fast, however. The U.S. count jumped from only 500 buildings in 2020 to more than 2,000 by 2023, indicating a rapidly expanding market.

Barriers remain in scaling the use of mass timber. Costs can be unpredictable, insurance hurdles persist, and many contractors are still inexperienced with the material. For developers, the question is no longer if timber will work, but when and where it makes sense. And while momentum is strong, lingering unknowns are holding some developers back.

This Insights by Blueprint report explores the uncertainties surrounding mass timber. Using a mix of market data, project case studies, and commentary from industry experts, it highlights the key forces affecting adoption, from cost and supply dynamics to design and insurance challenges. The goal is to provide developers and operators with guidance on:

- When projects are likely to pencil out

- How to navigate risks, and

- Which approaches set projects up for success

The forces driving mass timber forward

Cross-laminated timber (CLT), a wood panel building system, was first developed in Austria and Germany in the early 1990s. It didn’t reach North America until 2002, when Canadian researchers began studying it. By 2010, Nordic Structures, based in Quebec, had opened the first full-scale CLT plant in North America. The rest, as they say, is history.

Although CLT was pioneered in Europe, its use in North America has expanded steadily since the early 2010s. Designers and developers have been drawn to it for a mix of practical and aesthetic reasons: it performs well structurally, creates a unique interior look, and carries a much smaller carbon footprint than steel or concrete. Because CLT can serve simultaneously as a building’s frame, finish, and sustainable material choice, it has evolved from a niche option in commercial construction to a credible, increasingly common feature of projects.

Several converging factors have contributed to the rise of mass timber in the U.S.:

Code changes: The 2015 International Building Code formally recognized CLT, establishing product standards and design pathways for this material. Subsequent updates in 2021 and 2024 expanded allowances for taller buildings up to 18 stories.

Education initiatives: Woodworks has delivered more than 65,000 hours of training to architects, engineers, and contractors nationwide. Demand is surging at industry events, from Urban Land Institute’s fall meetings to specialized timber conferences, as CRE professionals seek guidance on how to design and deliver projects successfully.

Manufacturing expansion: In 2015, only a handful of Canadian producers supplied the U.S. market. Today, North America is home to a dozen major plants, with key players including Mercer, Element 5, Sterling, SmartLam, and Timberlab.

Adoption patterns have evolved in four distinct phases:

- 2015-2020: Office projects led the charge, most notably Hines’ T3 series, which demonstrated that mass timber could compete on cost across different markets.

- Pandemic years: The focus pivoted toward multifamily, particularly mid-rise and tall-wood projects. Milwaukee’s Ascent tower became the headline example. At 25 stories, it set a new record as the world’s tallest timber building.

- Recent growth: Universities, schools, and civic institutions have adopted timber, leveraging ESG and wellness benefits.

- Emerging frontiers: Developers are now exploring data centers, warehouses, and even healthcare as potential applications for mass timber.

Mass timber manufacturing in the U.S. grew out of the country’s strongest regional “wood baskets.” Two areas in particular became the foundation for production.

- In the Pacific Northwest, vast forest resources and a long history of sawmills created a natural hub.

- The Southeast also developed into a major cluster, with mills capable of supporting large-scale output.

Even though production is concentrated in these regions, wood’s relatively light weight makes it easy and economical to move. Softwood lumber from these hubs is routinely shipped long distances, reaching markets as far away as California and the Northeast.

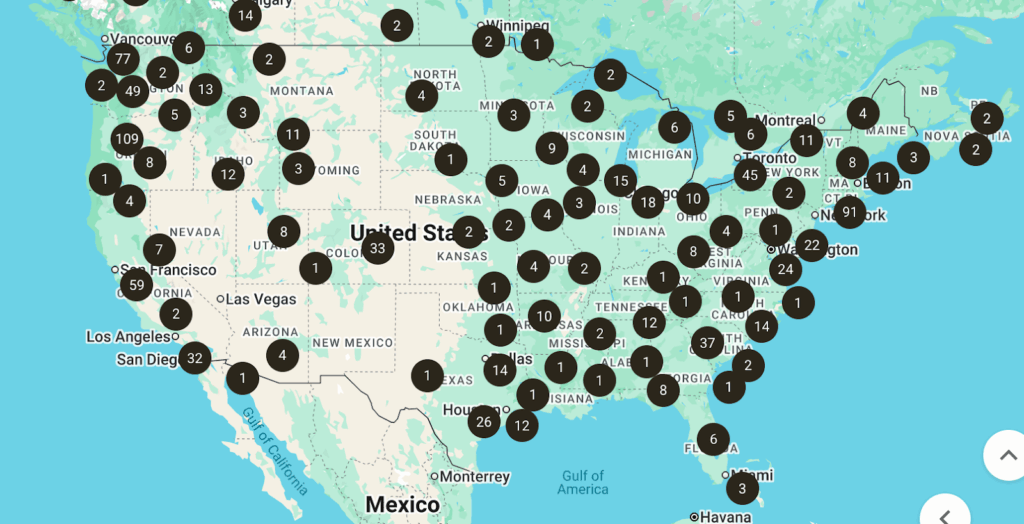

As a result, regionality has shifted from being about logistics to being more about adoption and education. As of August 2025, mass timber commercial developments are now more evenly spread across the continental U.S., with a steadily growing share on the East Coast, according to an interactive map from the Woodworks Innovation Network.

Source: Woodworks Innovation Network

The use of mass timber technologies has been driven by a select group of early adopters, including developers, architects, and contractors, who are most actively experimenting with the material. In this sense, geography has impacted who is building with mass timber, rather than where the material can be feasibly shipped or supplied.

Lessons from the world’s tallest timber building

The Ascent tower in Milwaukee is a milestone example of what tall mass timber construction can achieve. Rising 25 stories and reaching 284 feet, it currently holds the title of the world’s tallest timber building. Its design blends a concrete podium and cores with a timber structural frame, housing 259 apartments. Additionally, it features 7,000 square feet of retail space at street level and 20,000 square feet of resident amenities spread across the upper floors.

Finishing in 2022 was no small feat. The team spent more than two years working through approvals, securing 14 separate code variances and coordinating closely with city officials, engineers, and regulators. One of the most critical hurdles involved fire testing.

Partnering with the U.S. Forest Service and the Forest Products Laboratory in Wisconsin, the project subjected timber columns and beams to three continuous hours of exposure to an open flame. The material held firm, demonstrating structural integrity and opening the door for final permitting. That fire test set an important precedent, clearing a path for future tall timber projects nationwide.

Once approvals were in place, construction underscored the efficiency benefits of prefabricated timber. The project was finished in 22 months, about four months faster than a similar concrete tower. Prefabricated CLT and glulam components were CNC-cut with millimeter-level precision, arriving on-site ready to install. This approach reduced the need for large on-site crews and heavy concrete pours, lowering both labor intensity and neighborhood disruption. The building’s lighter weight also required a smaller foundation footprint, further reducing time and cost.

Market reception was strong. Ascent pre-leased quickly and achieved rents of $3.25 per square foot, above the $3.10 market average for comparable Class A multifamily in Milwaukee. Whether this premium is directly attributed to mass timber is harder to measure. Amenities, location, and design quality all played a role. Still, resident feedback consistently highlights the appeal of exposed timber aesthetics and biophilic design.

A ‘meaningfully different’ process

For Tim Gokhman, Managing Director of New Land Enterprises, whose firm co-developed Ascent with partner Wiechmann Enterprises, the project proved that mass timber is “meaningfully different” from conventional construction.

Gokhman says the difference lies not just in materials, but in process:

- Pre-construction precision: Every trade had to adapt to timber’s “no cushion” design logic, where digital models and CNC production eliminate the tolerance margins common in concrete and steel.

- Coordination demands: Success required dozens of additional pre-construction meetings to align MEP, fire suppression, and structural systems.

- Specialized expertise: Contractors and subcontractors needed training and guidance, highlighting the importance of having at least one experienced timber partner on a project team.

As Ascent has proven, tall timber projects offer real advantages, including faster schedules, distinctive marketing appeal, and alignment with ESG principles. But Gokhman cautions that they are complex projects and much different from traditional concrete or steel builds. Success depended on assembling an experienced team, budgeting significantly for early coordination, and preparing stakeholders for a different approach to building.

“There’s still a major knowledge gap around mass timber, and a lot of assumptions get made,” Gokhman said. “Legacy developers aren’t the ones taking this on. They already have enough problems. It’s mostly younger developers stepping in, but many lack the experience to understand how operations, cap rates, and investor expectations actually play out. That inexperience often turns into wishful thinking.”

The tricky economics of mass timber

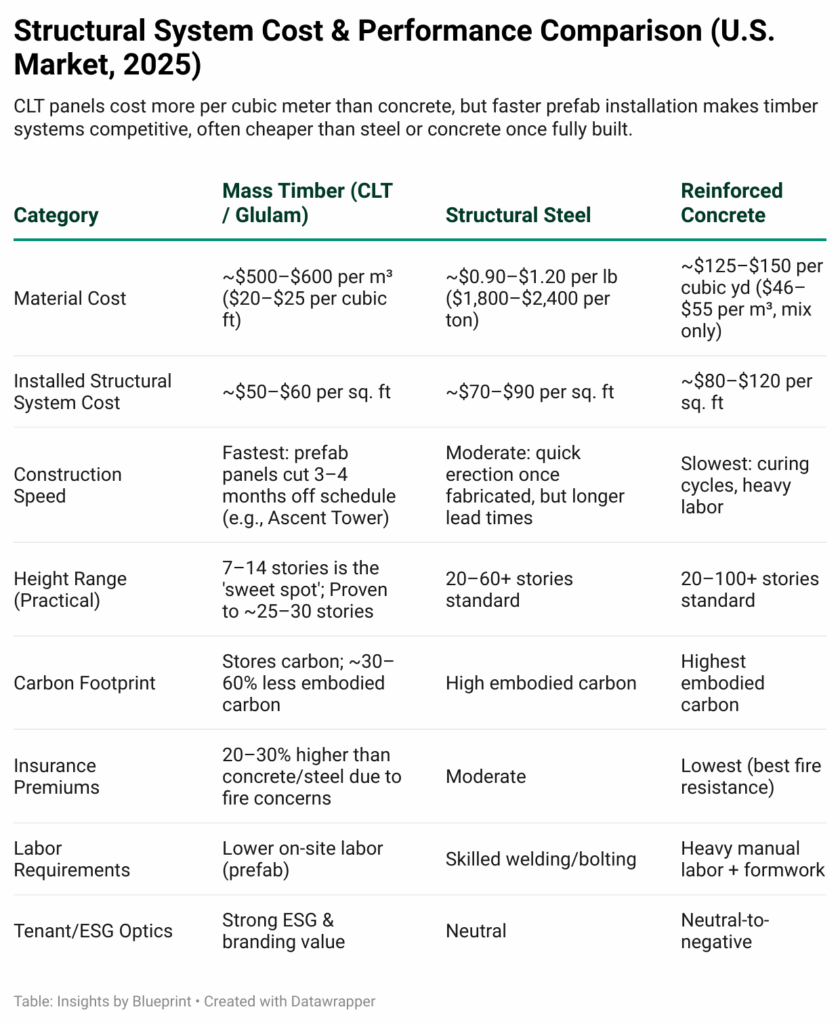

Cost is still the central sticking point when it comes to mass timber. Some developers provide examples of projects that came in at or below the cost of steel and concrete. Others point out higher material costs, difficulties with insurance, and unanswered questions about the material’s long-term performance. Both sides make valid points. In practice, the numbers depend on the type of project being built, the region where it’s being constructed, and the level of experience the project team has with timber.

Competing perspectives

Bill Parsons, COO of Woodworks, notes that mass timber has greatly reduced the cost gap with steel and concrete. On average, direct costs now fall only a few percentage points higher than steel or concrete. Once you factor in time savings from faster schedules, lower labor demands, and the potential to start collecting rent earlier, timber projects can hold their own, or even come out ahead, financially. A prime example is Hines’ T3 office portfolio. The company has repeated this concept in more than 20 buildings worldwide, consistently achieving rent levels and absorption rates strong enough to sustain reinvestment in timber.

According to Tim Gokhman of New Land Enterprises, cost is still the biggest hurdle for mass timber. Premiums often increase due to higher material prices, a lack of insurance precedent, and the additional care required for moisture protection. Just as important, many developers make errors in their pro formas. Some forget to budget for concrete cores, others underestimate soundproofing needs, and many assume tenants will pay more simply because a building is sustainable. Those kinds of mistakes skew the numbers, sometimes making timber look uncompetitive, and at other times creating expectations it can’t meet.

Takeaways

The biggest challenge is that the direct costs for mass timber are clear, but the benefits, such as faster lease-ups and rent premiums, are hypothetical and impossible to predict. While trade groups such as Woodworks argue that developers should model timber projects on a total project economics basis, this approach isn’t realistic and is prone to costly errors. Until there’s true, upfront cost parity with concrete and steel, most developers may be hesitant.

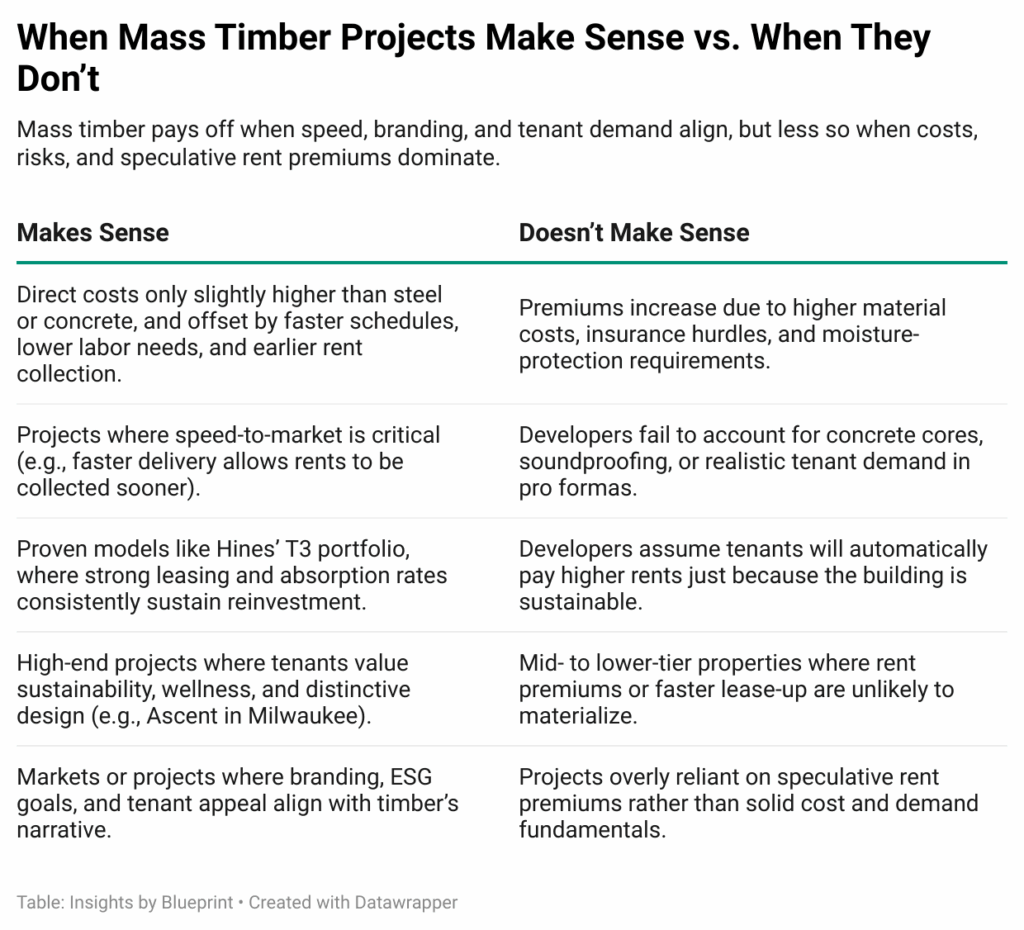

Since timber projects must be evaluated on a case-by-case basis, we have created a chart below that illustrates when timber projects may be viable and when they may not.

The evolving timber supply chain

The supply chain for mass timber appears significantly different today than it did just a few years ago. When the Ascent project in Milwaukee broke ground, the team imported panels from Austria. That dependence on overseas shipping left the project vulnerable to delays and disruptions, such as the Suez Canal blockage. Since then, North America has developed enough capacity of its own to stand as a reliable production hub.

Since 2015, the number of North American manufacturers has grown from a handful of Canadian producers to more than a dozen major players across the U.S. and Canada (see the locations of mass timber manufacturers and fabricators in North America here).

Companies such as Mercer, Element 5, Sterling, SmartLam, Timberlab, and Nordic Structures have brought new plants online, while Sumitomo has made a major investment in U.S. forestland and a new mill, signaling long-term confidence in the market. Notably, most of these facilities are still operating at a single shift, leaving untapped capacity that could be activated as demand scales.

Jamestown’s locally grown mass timber project

A recent project from Jamestown, the global real estate investment and management firm, shows the growth of the U.S. mass timber supply.

In 2024, Jamestown completed 619 Ponce, Georgia’s first mass timber project built from a regional supply chain. The building showcases southern yellow pine harvested, in part, from Jamestown-managed forests near Columbus, Georgia, processed at Georgia-Pacific’s Albany sawmill, fabricated into CLT panels and glulam beams at SmartLam’s Alabama plant, and erected on site at Ponce City Market by StructureCraft and JE Dunn.

By keeping the entire mass timber supply cycle of harvesting, milling, and fabrication within the region, Jamestown reduced transportation emissions, strengthened the local economy, and captured the full sustainability advantages of mass timber.

“We approached 619 Ponce as both a real estate project and an opportunity to prove a larger thesis: locally sourced timber can and should play a central role in the future of mass timber real estate development,” says Michael Phillips, Chairman and President of Jamestown.

When Jamestown started the project, Phillips says it was actually less expensive to source mass timber from Eastern Europe or the Pacific Northwest. There was even a bias in the industry against southern yellow pine because of its color compared to fir.

“We believed that the material grown in the South was not only viable, but culturally and aesthetically relevant,” Phillips says. “By investing in Forest Stewardship Council certification, learning the processing side, and piloting this project locally, we’ve shown that you can overcome those biases.”

With more than two-thirds of Georgia covered in forests, the Georgia Forestry Foundation says the state can regrow enough wood for an entire building in under 17 minutes. And because Jamestown and others manage their timber land sustainably, harvested acres are replanted, ensuring the cycle of renewable growth continues.

In testimony to the U.S. Agricultural Committee, Troy Harris, Jamestown’s Managing Director of Timberland and Innovative Wood Products, emphasized that over one-third of the U.S. is forested, and 67% of that land is managed as “working forests” that supply wood for everyday products. About 70% of these forests are privately owned, yet only 2% of private working forestland is harvested each year, and that same acreage is replanted or naturally regenerated.

These figures point to the strength and renewability of America’s forests. They also demonstrate how locally sourced timber, similar to Jamestown’s approach, can reduce dependence on imports while building a stronger, homegrown supply chain for real estate projects.

Global supply

European suppliers continue to play an important role, particularly in large projects that require consistent and reliable output. Austria and Germany remain at the forefront of global CLT and glulam production, and their extensive experience gives developers confidence in their supply. But relying on overseas shipments carries obvious risks. Delays at customs, container shortages, geopolitical instability, or sudden shifts in trade policies slow a project and add costs. That’s why U.S. developers are placing a greater emphasis on securing mass timber from domestic production and diversifying sourcing across multiple regions.

Resilience lessons

Some cite the failures of Katerra and Structurlam as a cautionary tale for mass timber suppliers. Both entered the market with ambitious plans but eventually went bankrupt. Bill Parsons of Woodworks says that these failures don’t indicate wider problems with mass timber suppliers as a whole, but they do highlight the need for careful vetting. Developers are now more likely to verify a supplier’s financial stability before making a commitment. On larger projects, it is common to divide orders among several suppliers to avoid overreliance.

Takeaways

The supply chain for mass timber in North America has undergone significant improvements over the past few years. It’s no longer the biggest barrier holding projects back, but it isn’t foolproof either. There’s enough production to handle larger builds, yet maintaining stability still comes down to carefully vetting suppliers and building trust early on.

The mass timber learning curve

Mass timber construction marks a significant cultural shift in the way buildings are conceived and delivered. To succeed, teams must adjust design tolerances, rework pre-construction processes, and invest in new approaches to training the workforce.

“Contractors and construction in general are slow to change,” says Bill Parsons, COO of Woodworks. “They’re part of the group around the table that really has to learn what mass timber is about and how to build with it.”

Architects are often enthusiastic about the aesthetic, and engineers are increasingly confident in their ability to design with timber. But contractors, unfamiliar with the systems, frequently bundle additional risk into their bids. “The contractor says, ‘I don’t know about this stuff, so I’m going to add a lot of risk,’” Parsons explains. This lack of experience has directly stalled projects, illustrating the cost of the industry’s education gap.

Organizations like Woodworks have recognized this challenge and are actively rolling out training programs. Their construction management curriculum, which will expand further in 2026, focuses not just on labor training but also on estimating and contractor-side expertise. The goal is to reduce the uncertainty that contractors bring to the table.

At the developer level, knowledge gaps also persist. While a few early adopters have adopted timber and worked to understand the material thoroughly, most developers remain hesitant. To bridge this divide, initiatives led by groups like the Urban Land Institute (ULI) have been crucial. Educational sessions at ULI’s fall and spring meetings have drawn packed rooms, but as Parsons notes, “It really has been a drop in the bucket. It’s just such a brand new thing.”

Like building with Legos

Mass timber’s strength lies in its precision. CNC (Computer Numerical Control) machines cut CLT panels and glulam beams to millimeter-level tolerances. This means structural components arrive on-site ready to slot together, more like a Lego system than a poured concrete frame. While this precision reduces field errors, it forces trades to abandon the “cushion” design assumptions that have long been standard in concrete and steel work. Plumbing, electrical, and mechanical systems must be modeled with complete accuracy upfront. There is little room for field improvisation once panels are delivered.

Coordination

The Ascent Tower in Milwaukee highlighted just how different mass timber construction can be. Tim Gokhman of New Land Enterprises, which co-developed the building, explains that the real challenge was coordinating the trades.

Gokhman says that with mass timber, you’re dealing with CNC machines, and they don’t make mistakes. “They’re very precise. And so the only mistake they’ll make is the one that the human puts in,” he says. “And getting trades to think about what a building process looks like, where every structural component can be relied upon to be within 3/16 of a millimeter in size, that’s much different than what most of them are used to.”

Openings for plumbing, HVAC, and fire systems had to be mapped out in 3D before fabrication, which meant dozens of extra planning meetings. “It was crazy how many pre-con meetings we had,” Gokhman recalls. That added time and cost at the start, but it made installation quicker on site. The process required a level of discipline the team hadn’t experienced before, and without that preparation, even minor design mistakes could have caused significant setbacks.

Training

The construction workforce is still finding its footing with mass timber. Some installers and fabricators have developed considerable expertise, but most contractors and subcontractors remain inexperienced. That gap often manifests as cautious bids, higher-risk pricing, or hesitation to take on projects at all. Trade groups are offering training and education to help close the gap, although participation varies. In many cases, it falls to the developer to explain what timber requires and guide teams through the process.

For owners and operators, the implications are clear:

- Budget for pre-construction: Expect more design meetings and coordination upfront than with conventional projects.

- Invest in training: Partner with trade groups to educate contractors and reduce risk premiums.

- Bring in experience: At least one team member—developer, architect, GC, or installer—should have prior timber experience.

- Over-communicate: Treat coordination not as an add-on, but as the central success factor for a timber project.

Takeaways

Mass timber can indeed deliver faster and cleaner builds with a high level of precision, but only if the project team adopts a different approach. Running it the same way you would a concrete or steel job doesn’t work. Success comes from treating the process more like a manufacturing operation, mapping out each step in advance, maintaining tight tolerances, and involving all trades early in the process. The developers who adapt in this way tend to realize the most substantial gains, from quicker schedules to reduced labor costs and stronger market positioning.

The insurance barrier

Insurance remains another stubborn headwind for timber projects. Unlike steel and concrete, there is no long historical record of fire-loss claims for mass timber at scale. This lack of actuarial data leaves carriers in the position of assigning risk premiums to cover uncertainty.

Two issues loom especially large:

- Moisture damage and repair costs — insurers are wary of prolonged water exposure during construction or from sprinkler activation, where hidden damage within panels can be costly to remediate.

- Uncharted scale — while low- and mid-rise projects have proven safe, tall timber still triggers a “first-of-its-kind” risk perception for many underwriters.

Blueprint recommendations:

- Engage insurers early. Don’t wait until underwriting. Bring carriers into design discussions to reduce perception gaps and align on risk-mitigation strategies.

- Leverage third-party fire and life-safety testing. Independent test data builds credibility and gives insurers tangible evidence to replace theoretical concerns.

- Build trust through peer examples. Highlight completed projects, especially those with successful claims histories, to normalize timber as a proven asset class.

The market’s appetite for mass timber

Multifamily renters often respond positively to the look and feel of mass timber. The exposed wood interiors and natural atmosphere give buildings a warmer character, and surveys show that younger tenants in particular link those qualities to health and sustainability. That said, most aren’t willing to pay a premium just for the green label.

The advantage shows up in other ways. Units tend to lease more quickly, and residents are more likely to renew their leases. For multifamily developers, timber works best as a differentiator in competitive markets rather than as a direct tool for raising rents.

Corporate office tenants

Office and institutional tenants have proven to be a steadier source of demand. Large companies, especially those in the Fortune 500 with ESG goals, WELL or LEED targets, and workplace wellness initiatives, see timber as both practical and brand-aligned.

These projects help reduce emissions while also sending a visible signal of progressive values to employees and stakeholders. In many cases, that interest translates into longer leases and stronger marketing appeal, particularly for firms competing to recruit and keep top talent. Framing timber as part of a “future-ready workplace” story tends to resonate more than simply emphasizing technical sustainability points.

Investors

Capital remains the most cautious part of the equation. Traditional institutional investors may be reluctant due to the limited operating history of tall timber assets, concerns about liquidity, and perceived construction risk. By contrast, emerging funds and entrepreneurial developers, often those with mandates to differentiate through ESG, are stepping in earlier.

These first movers see an opportunity to capture premium tenants and establish themselves as category leaders. Legacy players remain watchful, waiting for more stable portfolios and benchmark returns before scaling exposure.

The first-mover advantage

Mass timber is entering a new phase of expansion. While the current capital market slowdown has tempered development pipelines, the underlying fundamentals suggest a rebound. Once financing conditions ease, Parsons of Woodworks estimates that the use of the material will return to a year-over-year growth rate of 20–30%, a pace similar to that seen before interest rate hikes constrained activity.

This growth will likely be driven by both repeat adopters who have already navigated early challenges and new entrants drawn by proven case studies. The Chamber of Progress states that projections forecast 24,000 new timber commercial structures will be built by 2034. Major firms, such as Walmart, Meta, and Google, are integrating mass timber into new developments, including Walmart’s new HQ campus in Bentonville, Arkansas.

For some design firms, mass timber has become an essential component. Global architecture firm Pickard Chilton’s first mass timber design was completed in 2018, the ATCO Commercial Centre in Calgary. Michael Hensley, who leads Pickard Chilton’s mass timber research initiative, says that at the time, the use of timber was treated as a special consideration.

Since then, Pickard Chilton has designed four million gross square feet of timber architecture across North America. Today, the firm evaluates timber as a standard option on nearly every project, reflecting broader market maturity and client demand.

Hensley says that during the Calgary project, timber felt a bit exotic. “The big shift now is realizing it doesn’t have to be reserved for signature buildings,” he says. “It can work across an entire portfolio, with different strategies for integration. We even recently explored a full timber campus for a California tech company.”

Pickard Chilton has learned to integrate timber cleanly with MEP systems, reducing clutter and preserving the warmth of exposed wood while improving construction efficiency. Even when full timber structures aren’t feasible, Hensley says hybrid solutions, like timber pavilions within steel towers, deliver leasing advantages, tenant appeal, and a strong sustainability narrative.

Developers who invest in supply chain partnerships and contractor training today can still enjoy a first-mover advantage. As timber moves into the mainstream, those already fluent in design coordination, insurance negotiations, and procurement will be able to scale portfolios quickly while late entrants scramble to catch up.

Final takeaways

The past decade has seen steady growth in mass timber projects, a maturing North American supply chain, and expanding acceptance from regulators, tenants, and financiers. Yet the industry is still in its formative stages in the U.S. Costs remain variable, insurers are cautious, and contractors are unevenly trained.

The central lesson is clear: mass timber succeeds not by imitating steel and concrete workflows, but by rethinking the development process. Early coordination, supply chain diligence, and insurer engagement are the price of admission for a material that rewards precision and foresight. Mass timber is a powerful new tool in the U.S. developer’s playbook. Those who treat it as such will be positioned not just to deliver singular projects, but to define the next era of building.

– Nick Pipitone