AI is reshaping many corners of multifamily operations, but its limits are just as revealing. Nowhere is that clearer than in insurance claims automation.

Insurance remains one of multifamily’s most stubborn and least-optimized operational problems. AI-driven insurance platforms promise a fix. Vendors pitch automated claim intake, faster documentation review, and portfolio-level risk scoring that can flag problems before they turn into losses.

Multifamily operators remain unconvinced, for now.

Exclusive survey data from the Insights by Blueprint Advisory Council shows that operators clearly understand the source of insurance pain. But most are not persuaded that today’s AI-driven claims tools deliver enough near-term value to justify the cost, integration effort, and organizational change required. This report examines where AI-driven insurance tools are gaining traction in multifamily, where they fall short, and why many operators remain firmly in wait-and-see mode.

Why multifamily isn’t rushing to automate claims

AI-driven insurance platforms have the potential to change how multifamily claims are handled by automating claim intake and categorization for common incidents such as water damage and resident liability.

Some systems can review photos, videos, work orders, and invoices to flag missing or inconsistent documentation, helping operators submit more complete claims upfront.

For onsite teams, this can reduce administrative burden and streamline the path from incident to claim submission.

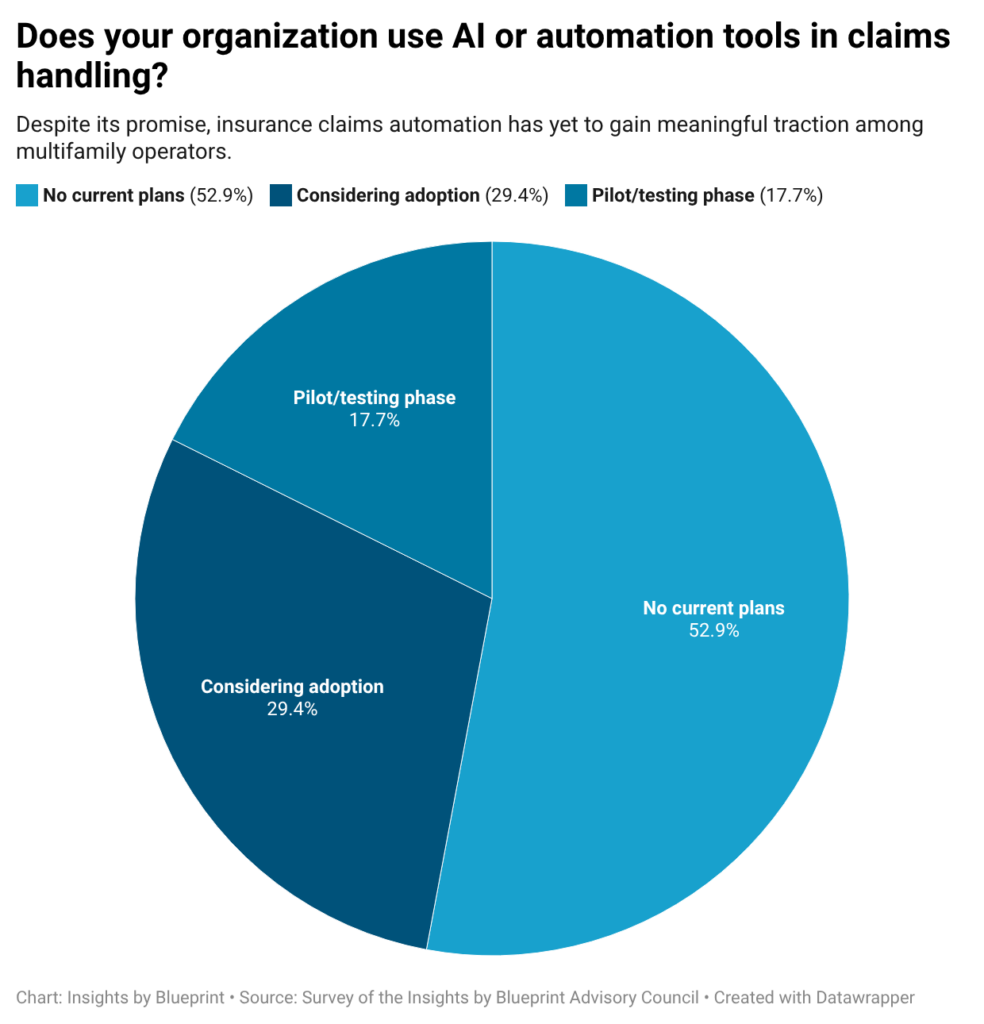

But despite these potential efficiencies, adoption remains limited. In a survey of the Insights by Blueprint Advisory Council, 53% of respondents said they have no current plans to use AI or automation tools for claims handling. Another 29% said they’re considering adoption, while just 18% are actively piloting or testing such tools.

There are a few reasons why multifamily operators aren’t rushing to automate claims:

ROI is hard to prove at low claim volumes

For many portfolios, insurance claims are painful but not always frequent enough to justify new software spend. Operators with relatively low claim volumes struggle to see clear, near-term ROI, especially when savings are incremental rather than transformational.

Claims workflows are highly variable

Unlike leasing or accounting, insurance claims vary widely by incident type, carrier requirements, jurisdiction, and property condition. Operators worry that rigid automation forces “square-peg, round-hole” workflows that create more friction than they remove.

Documentation starts with onsite teams

AI tools can only work with the data they’re given.

Documentation quality depends on onsite staff taking consistent photos, writing clear notes, and promptly uploading records. Many operators see documentation standardization, not AI, as the real bottleneck.

Integration adds complexity, not simplicity

Claims automation tools often sit outside core property management and maintenance systems.

Without clean integrations, operators risk duplicative workflows, manual reconciliation, or fragmented records. This undermines the efficiency gains the tools promise.

Insurance isn’t a top operational priority

Despite rising premiums, insurance automation competes with higher-visibility initiatives like leasing, revenue management, maintenance, and resident experience. Claims are episodic, making them harder to prioritize amid constant operational demands.

Vendor maturity remains uneven

Operators report difficulty finding products that fit their portfolio size, claim profile, and internal processes. Many tools feel either too narrow to matter or too complex to deploy, reinforcing a wait-and-see posture.

Internal process fixes often come first

Some operators believe the best ROI comes from fixing claims processes internally by standardizing intake, defining required documentation, and clarifying roles before layering in AI. Automation is viewed as a second step rather than a starting point.

Early use cases, mixed impact

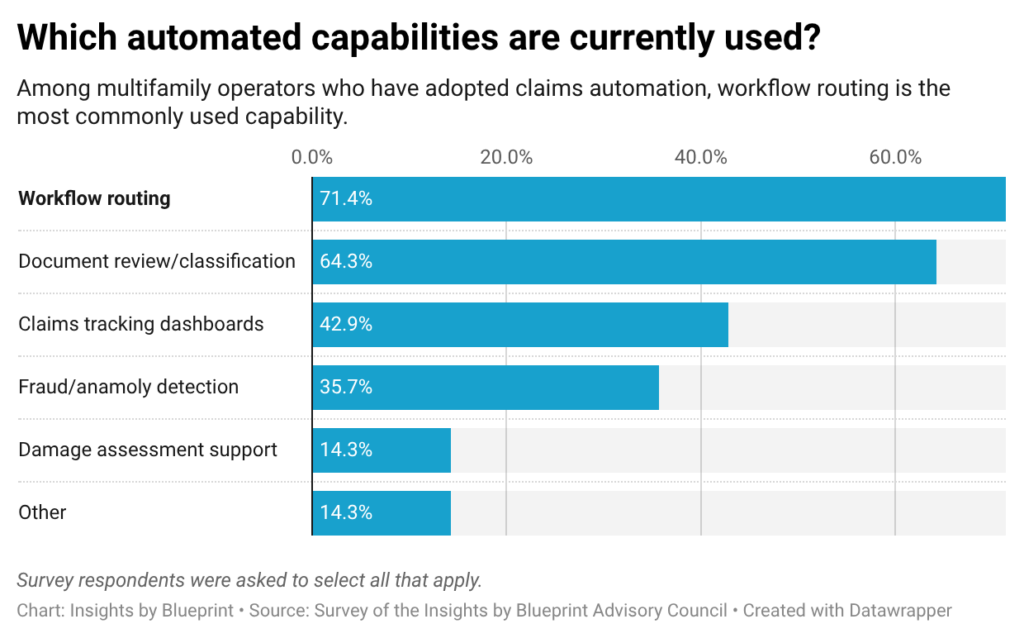

Among the relatively small group of operators currently piloting or using AI for claims automation (18% of survey respondents), adoption has clustered around a handful of practical, low-risk use cases.

Within that group, 71% report using AI for workflow routing and 64% for document review and classification. These applications streamline administrative tasks without fundamentally changing how claims decisions are made.

Fewer operators report using AI for claims-tracking dashboards (43%) or fraud and anomaly detection (36%), and only 14% apply AI to damage assessment, one of the more complex and judgment-intensive use cases.

Workflow routing, the most common application, refers to using AI to triage insurance claims and automatically direct them to the appropriate people, teams, or systems.

It can prioritize incidents, route documentation, and reduce administrative bottlenecks without making coverage determinations.

Because it improves process efficiency rather than replacing human judgment, operators tend to view it as a lower-risk entry point for AI adoption.

Even among adopters, results remain uneven.

Among operators currently using AI for claims automation, 47% cite reduced administrative workload as the primary benefit. About one-third (33%) report faster claims resolution. Smaller shares point to improvements in documentation accuracy (27%) and insurer coordination (27%).

At the same time, 47% of current users say they have not yet seen measurable portfolio-level impact.

Reduced administrative workload stands out because it delivers immediate, visible relief to onsite teams. Most AI claims tools focus on automating intake, documentation review, and follow-up tasks, areas where labor savings are quickly felt.

By contrast, improvements in financial outcomes, insurer coordination, or long-term loss performance require higher claim volumes and more time to evaluate.

This dynamic helps explain why some operators report operational efficiencies but remain unconvinced about broader ROI.

Despite experimentation, formal vendor relationships remain rare.

Only 6% of total survey respondents report currently working with a dedicated third-party AI claims vendor. While 18% are piloting or testing some form of AI claims automation, many of those initiatives involve internal tools, carrier-provided systems, or limited trials rather than full vendor deployments.

‘Square peg, round hole’

Overall, multifamily operators on the Insights by Blueprint Advisory Council remain cautious about AI-powered claims automation.

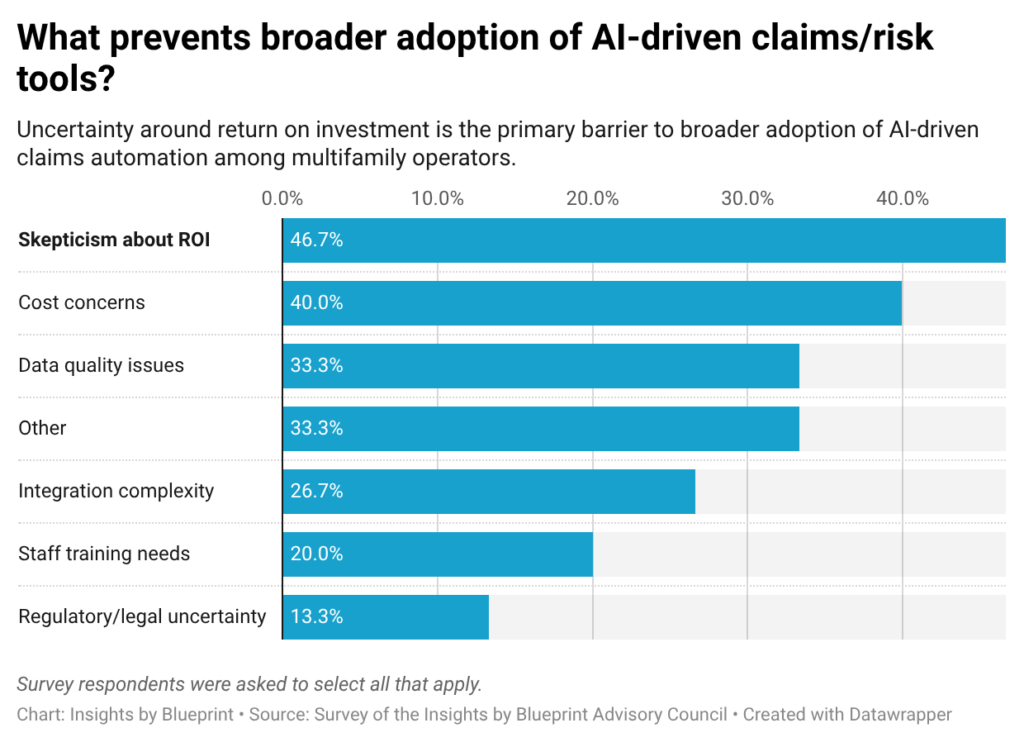

Survey responses indicate skepticism about near-term payoff. When asked what is holding back adoption, 47% cited uncertainty around return on investment, followed by cost concerns (40%), data quality limitations (33%), and the complexity of integrating these tools with existing systems (27%).

For many operators, insurance automation competes with higher-priority operational initiatives. Some respondents noted relatively low claim volumes, which makes it difficult to justify automation. Others questioned whether today’s vendor offerings are mature enough for real-world multifamily workflows.

One operator noted that although they have struggled to find the right product fit and implementation approach, insurance AI remains on their roadmap, with potential deployment planned for the first half of 2026.

Even among operators already using AI-driven insurance tools, enthusiasm is measured. The largest share (38%) described ROI as moderate, while 31% said they are uncertain. Nineteen percent reported high returns, and 12% characterized ROI as low. (Totals may not equal 100% due to rounding.)

Several operators suggested that internal process improvements may offer better returns than off-the-shelf automation. “Building something internally may be your best ROI option,” one respondent wrote, noting that the real challenge is automating existing claims processes.

Another advised starting small by mapping current workflows, standardizing digital intake requirements, and piloting AI-powered triage on a single claim type before scaling.

Others were more blunt. “Claims vary too much,” one operator cautioned. “Trying to force them into a system feels like a square peg in a round hole.”

Watching, testing, waiting

Claims automation can deliver clear value in narrow, well-defined use cases. But most operators have yet to see results compelling enough to justify broad deployment.

Adoption is low, returns feel uncertain, and many operators remain concerned about cost, data quality, and whether the tools actually fit into their day-to-day operations.

For now, insurance AI in multifamily is still unproven. Most operators are keeping an eye on it, testing it in small ways, and waiting to see clear proof that it works smoothly with their systems and delivers real value across their portfolios.

– Nick Pipitone