Revenue management platforms ingest massive amounts of data and then generate rent recommendations that, in many cases, no human analyst can match in speed or consistency. For operators managing hundreds or thousands of units across multiple markets, the appeal is obvious. Pricing has always been part art, part science. These tools tip the balance decisively toward science.

The reality, as our new Insights by Blueprint Advisory Council survey reveals, is more complicated. Adoption is widespread but not uniform. Performance gains are real but modest, with most users reporting incremental improvement rather than the step change in NOI that the technology promises. And the confidence that once surrounded algorithmic recommendations has recently given way to a more cautious outlook. Operators are cross-checking outputs, documenting their rationale, and keeping human judgment in the loop in ways they might not have before the RealPage settlement.

That shift is partly a product of market conditions, partly a response to legal and regulatory pressure, and partly a more sober assessment of what these systems can and cannot actually deliver. This report explores all three dimensions, drawing on data from the Advisory Council survey and insights from operators, legal experts, and industry observers.

Second-guessing outputs in a softening market

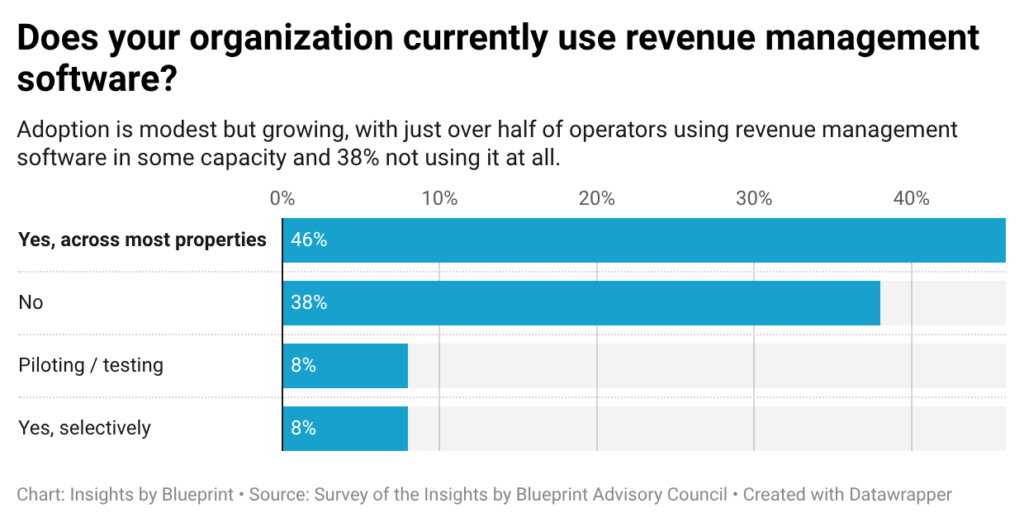

Adoption of revenue management systems across the multifamily sector is significant but far from universal, according to our survey of the Insights by Blueprint Advisory Council. Roughly 54% of operators report using these platforms across most of their properties, while 15% are running selective pilots or limited deployments. That leaves 38% not using them at all. It’s a split that reflects a market still in the middle of a technology adoption curve rather than one that has reached consensus.

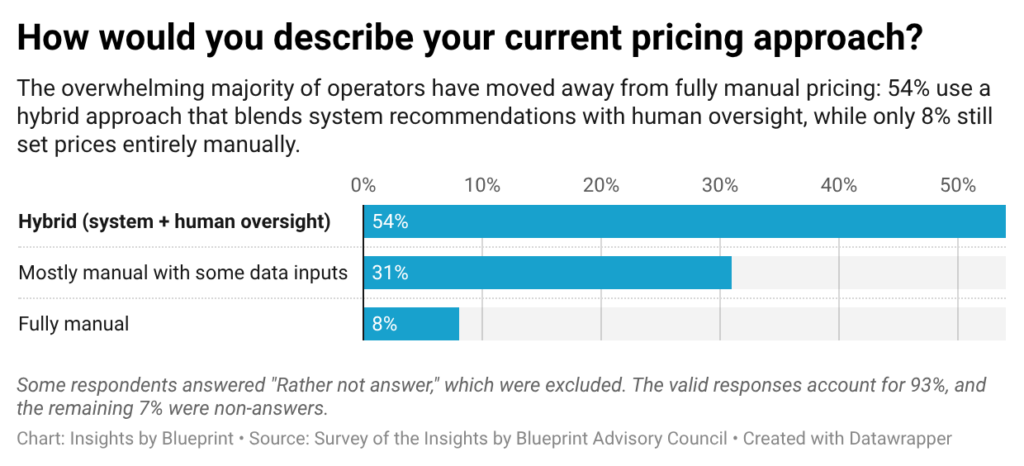

Even among those using the systems, full automation remains off the table. The dominant model is hybrid. Fifty-four percent of operators combine system recommendations with human oversight, and 31% describe their approach as mostly manual. Not a single respondent reported running fully automated pricing. The data is unambiguous: no one is handing control entirely to an algorithm. The performance picture tempers whatever optimism surrounds adoption. A majority, 62%, report moderate improvement in outcomes from using revenue management systems, while 23% have seen no change and 8% report a decline. Notably, no operators reported significant NOI growth. The honest read of that data is that these systems are delivering incremental gains, not step-changes in financial performance.

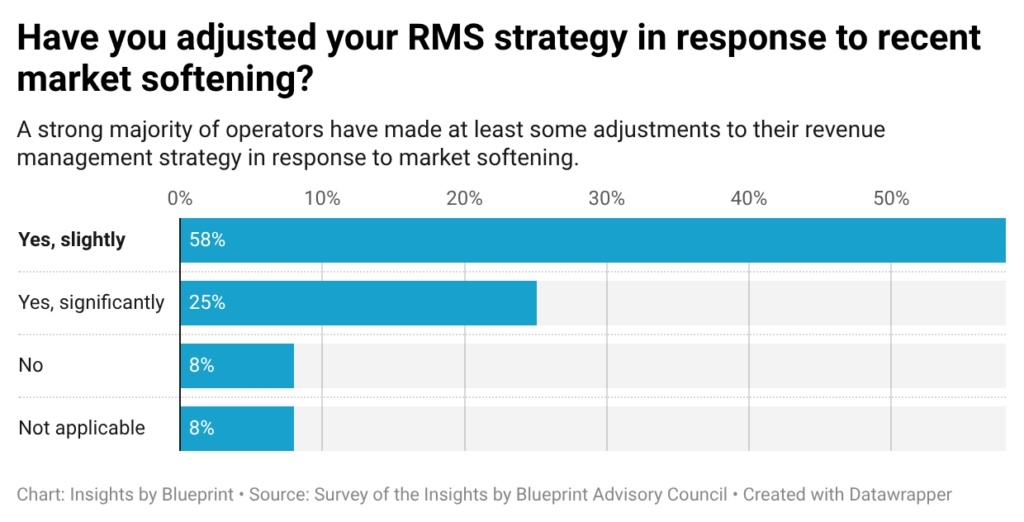

The current multifamily leasing environment is putting pressure on how operators use these tools. Seventy-seven percent of respondents say they have adjusted their revenue management strategy in response to market softening. Most describe those adjustments as moderate recalibrations rather than wholesale overhauls. The implication is that operators are actively overriding or second-guessing system outputs in softer conditions, reinforcing the pattern of human judgment taking precedence over algorithmic recommendations.

The core fear: Overpricing into vacancy

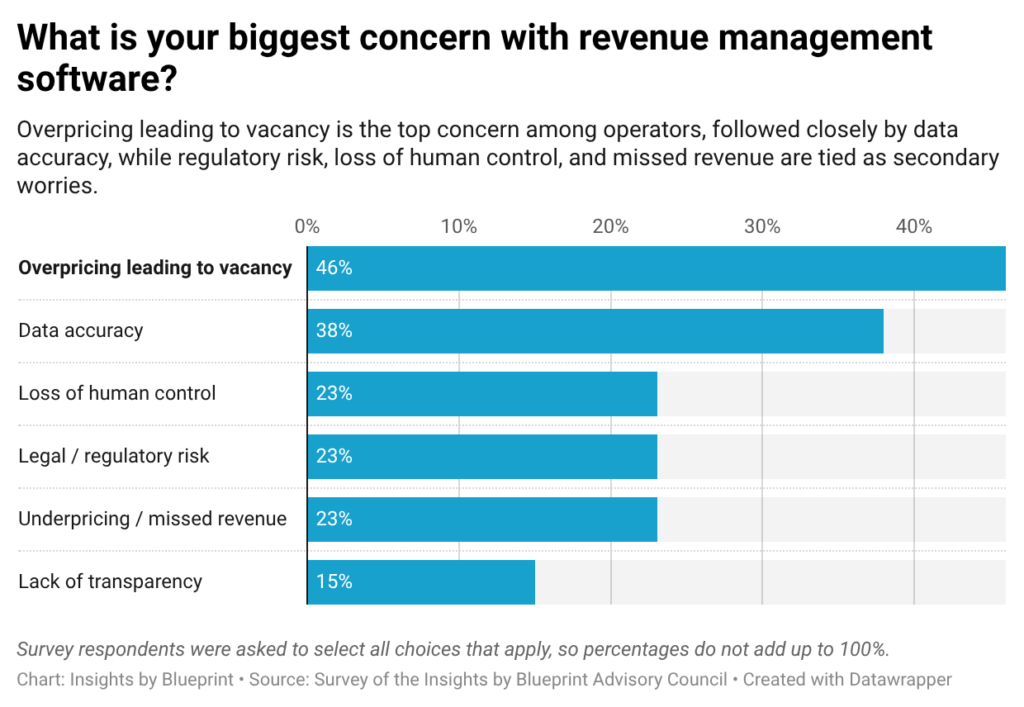

When asked about their biggest concerns with revenue management systems, overpricing leading to vacancy ranked as the top worry, scoring well ahead of data accuracy concerns, underpricing, legal risk, and loss of control. The dominant fear is that aggressive pricing will drive vacancy and erode revenue. That hierarchy of concerns directly reflects the current environment. In a softer leasing market, the tolerance for pushing rents beyond what the market will bear has dropped. Operators are more focused on keeping units occupied than on extracting maximum rent from each lease, and their concerns about the technology mirror that shift in priorities. Awareness of regulatory risk is widespread. Sixty-nine percent of respondents describe themselves as somewhat or very concerned about the legal and regulatory landscape surrounding algorithmic pricing. Only 23% report no concern at all.

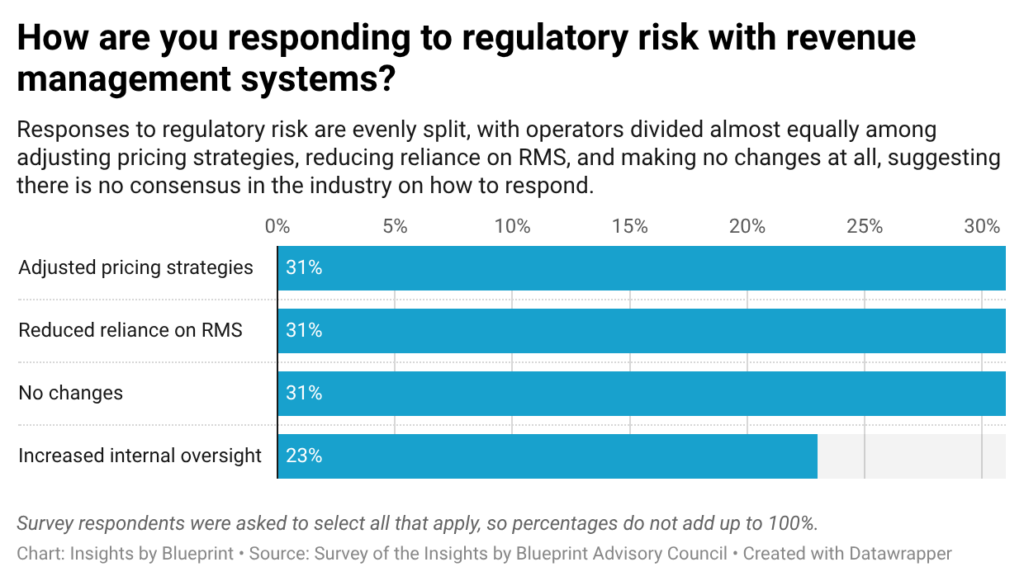

But concern has not yet translated into decisive action. Among those who have responded to regulatory risk, the split is essentially even. Some operators have adjusted their pricing approach, some have reduced their reliance on revenue management systems, and others have made no changes at all. There is no consensus strategy emerging. Operators are watching the regulatory environment, running experiments at the margins, and waiting to see how enforcement evolves. But few are making drastic moves. The gap between stated concern and actual behavior change remains wide.

Automation as advisor, not decision-maker

As our survey revealed, operators continue to use revenue management platforms, but the systems aren’t treated as the final word. They probably never were. Property managers routinely cross-check and review algorithmic suggestions before acting on them. “These existing systems are like guides in making the final decision,” said Jeff Burker, an Associate Broker at eXp Realty. “Operators don’t fully trust the suggestions, and they cross-check and review them. It’s like using manual control while still relying on the data for support. Information as an aid, not as the basis of final results.” Burke also notes a preference emerging for simpler, more explainable systems whose outputs teams can positively defend rather than opaque optimizers whose recommendations require faith rather than understanding. The emphasis has shifted toward stronger governance: clear, approved workflows, a documented pricing rationale, and a deliberate separation between input data and final pricing authority.

Your approval history is a paper trail

Michael Kruse, a criminal defense lawyer whose practice area includes business and corporate law, offers a more pointed warning. The industry’s focus on vendor selection, he argues, is misplaced. The real risk lies not in which platform an operator uses, but in how individuals within the organization engage with its outputs. “The operators who are switching revenue management vendors are dealing with this from completely the wrong perspective. Vendors are not the issue in price-fixing investigations. It’s the people that have reviewed the outputs and acted on them that prosecutors build a case against,” Kruse said.

Drawing on his experience on the prosecution side of major cases, Kruse explains that every email, meeting note, and documented sign-off supporting a pricing decision becomes potential evidence in establishing liability. The dynamic is compounded by corporate structure. Courts examine whether an individual had the authority to reject an algorithmic recommendation, and in most organizations, they do. Having the authority to override a system and not exercising it, Kruse argues, is itself a form of accountability. “Those operators that approved algorithmic outputs without the benefit of a manual review process and documented oversight are going to find themselves in a much more exposed position than currently believed,” Kruse said.

AI-driven pricing isn’t going away

Martin Orefice, CEO of Rent To Own Labs, takes a longer view. While the RealPage settlement represented a setback for automated pricing platforms, he sees the regulatory impact as limited. That’s partly because the tools are becoming increasingly accessible outside of dedicated platforms. “It’s possible to DIY these kinds of price comparisons with generic AI tools, and it’s only a matter of time before new platforms hit the market,” Orefice said. The enforcement actions that targeted RealPage may succeed in disciplining one platform while the underlying capability disperses across the market. The regulatory challenge, in Orefice’s framing, resembles whack-a-mole, containable at the margins but not at the root.

The revenue management vendor landscape

The revenue management vendor landscape is split broadly into enterprise suites, mid-market all-in-ones, and specialized standalone tools. RealPage is the dominant dedicated revenue management vendor, using its AI Revenue Management platform — formerly known as YieldStar — to optimize pricing and occupancy across large portfolios. It offers the most robust analytics in the space but has faced significant legal consequences over allegations that its algorithmic pricing facilitated rent coordination among competing landlords, culminating in a 2025 DOJ settlement that imposed three years of monitoring and new restrictions on how it collects and uses competitor data. Yardi Systems embeds revenue management within its broader Voyager platform through its Revenue IQ product, making it a natural choice for operators already running on the Yardi stack. It is the default system for many large national operators and REITs, valued for its depth of financial reporting and compliance tooling.

MRI Software takes a more modular approach through its MRI Living platform, appealing to operators who prefer a best-of-breed architecture with strong third-party integrations rather than a single locked ecosystem. Entrata bundles it into a growing all-in-one suite with strong automation capabilities. ResMan is a solid end-to-end option popular with regional operators who find enterprise platforms more than they need. On the specialized side, Rentana, LeaseMax (by Beekin), and REBA Rent are all standalone revenue management tools that integrate with existing property management systems. They have gained traction among operators seeking greater pricing transparency, faster implementation, and a credible alternative to incumbent platforms, especially in the wake of regulatory scrutiny of RealPage.

ApartmentIQ is a multifamily market data platform that has extended into revenue management through its Daylight product. Built on a dataset of over 16 million leases — drawn from its broader platform covering 37 million units — it positions itself as a post-RealPage alternative, using only public data to sidestep the antitrust concerns that have dogged legacy platforms. Explainability is a central selling point, with the system designed to provide a stated rationale for every pricing recommendation rather than a black-box output. It fits the standalone specialist profile, differentiating from RealPage and Yardi on transparency and data integrity rather than platform breadth.

For most operators, platform choice comes down to portfolio size and what they already run. Large portfolios tend to land on RealPage or Yardi. Mid-market operators often choose AppFolio or Entrata. Those wanting a dedicated revenue management layer without switching their PMS are increasingly turning to standalone specialists.

Trust, but verify (and document)

Revenue management systems have become a fixture of multifamily operations, but the picture that emerges from our survey is one of cautious, qualified adoption rather than wholesale embrace. Operators are using these tools regularly, overriding them, worrying about their legal exposure, and questioning whether the performance gains justify the complexity.

The RealPage settlement didn’t kill algorithmic pricing; it complicated it. It forced a more deliberate posture with documented rationale, manual review, and human accountability at every step. Whether that discipline holds as new platforms emerge and AI capabilities become easier to access outside of dedicated systems remains an open question. What’s clear is that the era of treating algorithmic recommendations as a black box is over. The operators best positioned going forward will be those who treat revenue management as a decision-support layer — one input among many, subject to scrutiny, and backed by a defensible process. The tools are not going away. The question is whether the governance catches up.

– Nick Pipitone

Got tips or feedback? Email Nick at [email protected]