A recent Insights by Blueprint Advisory Council survey found that 80% of multifamily respondents operate a centralized or partially centralized operating model. Not a single respondent in our survey described a model that has reversed course on centralization. But while the direction is fixed, the execution is not.

What has changed in the past eighteen months is the distance between what technology enables and what most organizations have built to deploy it. Artificial intelligence leasing assistants are now a core tool for 60% of surveyed multifamily operators. Virtual leasing concierges, centralized maintenance triage platforms, and portfolio-wide performance intelligence tools are commercially mature and widely adopted. But the organizational design, training infrastructure, and incentive structures needed to use these tools effectively have not kept pace.

This report examines the current state of multifamily centralization, drawing on Advisory Council survey data, operator research, and practitioner perspectives shared through mid-2026. It introduces a playbook for thinking about centralization as a decision architecture rather than a binary operational choice, and provides implementation guidance for operators at every stage of the transition.

Committed to centralization, cautious about speed

Our survey of the Insights by Blueprint Advisory Council showed the multifamily industry skewing toward the middle of the centralization spectrum. Thirty percent of respondents describe their model as partially centralized, 20% as hybrid or in transition, 20% as fully on-site, 10% as fully centralized, and 10% as primarily self-guided. No respondent described a model that had reversed course on centralization, which is consistent with the broader industry pattern: operators are debating pace and scope, not direction.

The drivers are consistent. Improving consistency across properties and reducing labor costs were each cited by 50% of respondents as primary drivers, making them the dominant motivators by a significant margin. Enabling portfolio growth without adding headcount came in at 30%. Staffing shortages and tech availability each appeared at 20%. The finding on consistency is notable: it suggests that the operational case for centralization is at least as compelling to this group as the cost case.

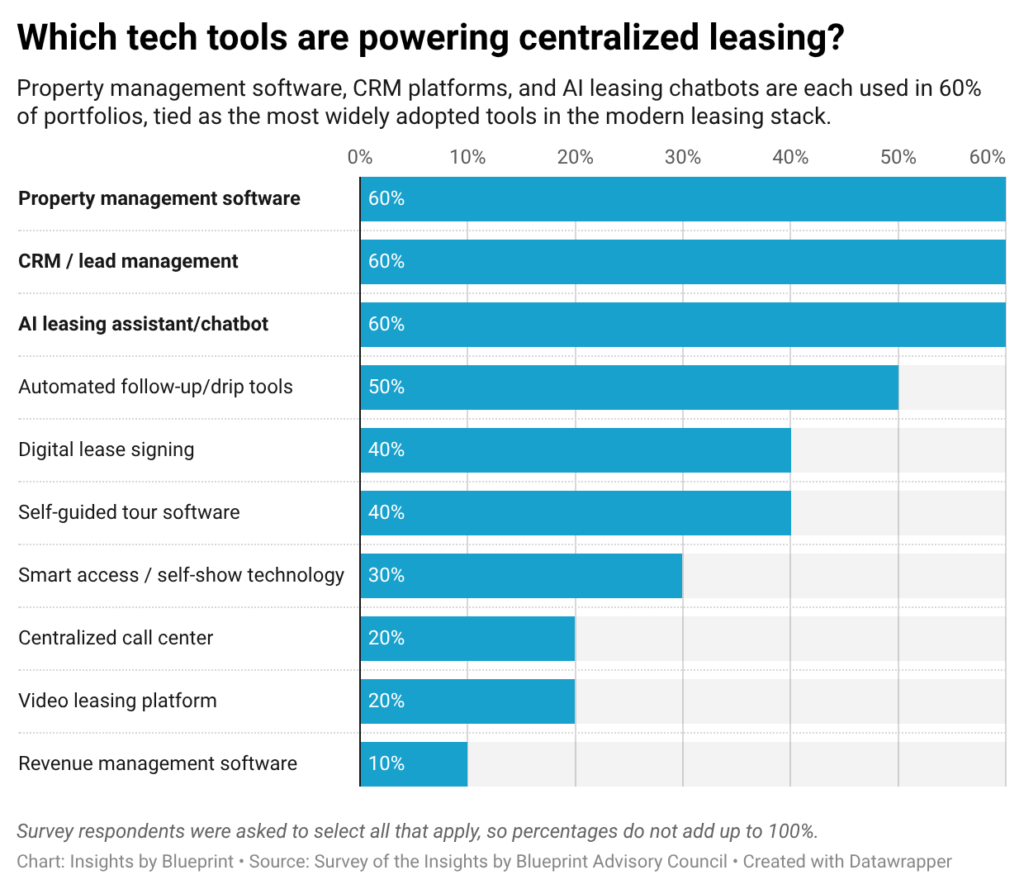

The tool stack is more mature than expected. Property management software and CRM or lead management platforms are near-universal, with 70% of respondents citing them. AI leasing assistants and automated follow-up tools are each deployed by 60%. It’s a high adoption rate and consistent with the industry trend of AI becoming core leasing infrastructure rather than an experimental add-on. Digital lease signing and self-guided tour software each appear at 50%. Revenue management software is a notable gap, appearing in only 20% of responses, suggesting that the integration between centralized leasing operations and dynamic pricing remains underdeveloped in many organizations.

What operators expect next

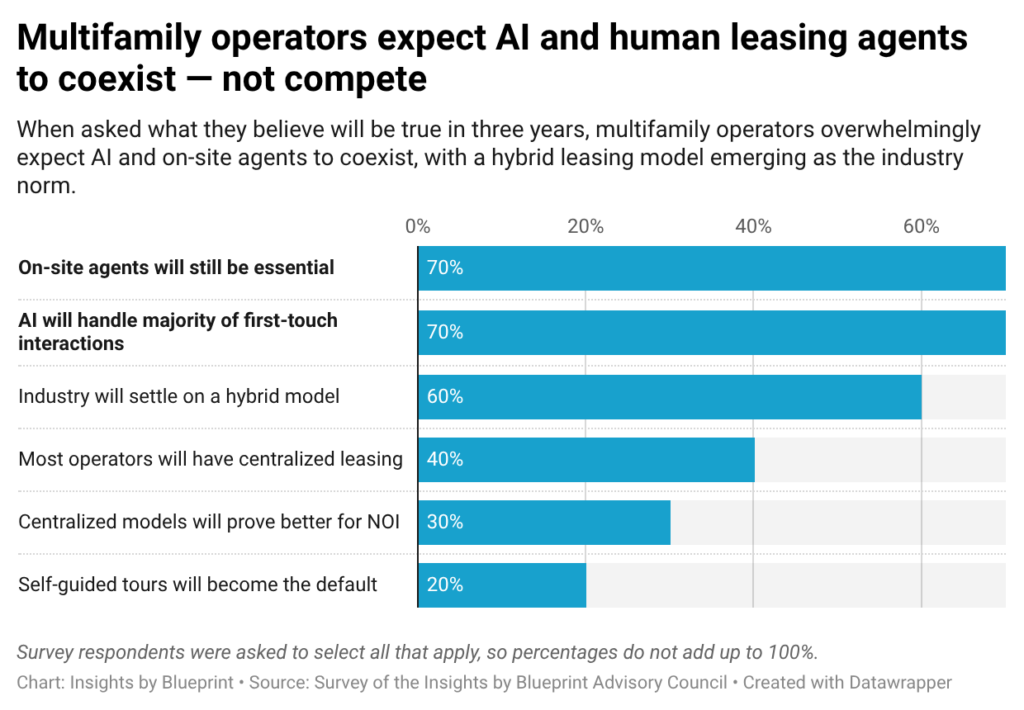

The most interesting finding in the survey is the three-year outlook. 70% of respondents believe on-site leasing agents will remain essential at most properties. Seventy percent also believe AI will handle the majority of first-touch prospect interactions. Sixty percent of respondents expect the industry to settle on a hybrid model as the norm. These three views describe the tiered centralization model that the most operationally sophisticated multifamily organizations are building: AI and centralized teams handle routine, high-volume interactions, while on-site staff remains present for high-judgment, relationship-intensive moments.

The views that attracted less consensus are equally instructive. Only 40% of respondents believe most multifamily operators will have centralized leasing within three years, and only 30% believe centralized models will prove better for NOI. These lower numbers do not necessarily indicate skepticism about the value of centralization. Instead, they indicate appropriate caution about pace and proof. Operators on the Advisory Council have consistently noted that the NOI case for centralization is real but slower to materialize than projected, and that organizations claiming large efficiency gains early in a transition are often measuring cost reductions before resident experience and conversion impacts are fully visible.

Centralization is harder than the headlines suggest

Several converging dynamics have made centralization both more attractive and more contested in the past eighteen months:

The third-party management complication. The multifamily industry’s shift toward third-party management has complicated the discussion of centralization in ways that are only now beginning to receive serious attention. Research published by 20for20 in early 2025, based on deep-dive interviews with fourteen third-party managers and ten asset managers from large institutional owners, documented a structural constraint that owner-operators rarely face: every centralization decision at a third-party-managed property requires an amendment to the property management agreement governing that asset. Where a REIT can redeploy leasing resources across a regional cluster with an internal operational decision, a third-party manager must negotiate each change with a separate ownership group.

The result is that centralization in the third-party context tends to take a property-by-property shape rather than a portfolio-wide one. That is a much higher bar to clear, and one that limits the scale benefits operators are seeking. That said, the research also documents how the most sophisticated third-party managers are finding paths through that constraint, including restructuring commercial arrangements with owners and piloting centralized services on owned assets before extending them to managed properties.

AI tooling has outpaced organizational design. The tech stack supporting centralized leasing has expanded rapidly. Platforms offering AI-assisted lead response, automated tour scheduling, virtual leasing concierges, and natural language triage for maintenance requests are now widely deployed. Companies like Funnel, HappyCo, and a growing field of newer entrants have built products specifically designed to support centralized operating models. HappyCo’s Joy AI engine, showcased at NAA Apartmentalize 2025 and deployed across more than 5.5 million units, enables centralized teams to ask direct operational questions and receive contextual answers drawn from actual service record data. According to HappyCo, operators on the platform are completing unit turns three times as fast and achieving technician-to-unit ratios as high as 1:170. The tooling, in other words, is now sophisticated enough to support meaningful centralization. The gap is the organizational design, training infrastructure, and incentive structures needed to deploy that technology effectively.

63% of operators plan to expand centralization within five years — and the more recent data suggests the number is higher. An NAA research report sponsored by MRI Software found that nearly two-thirds of multifamily operators intend to expand centralized operations within the next five years, while only 11% rate centralization as a highly significant operational challenge. MRI’s more recent 2026 Multifamily Real Estate Pulse Check, based on more than 700 responses from real estate professionals across North America, tells a sharper story: 87% of respondents plan to increase centralization in the next 12 months.

That figure, however, sits alongside a striking set of concerns. 85% worry that centralization will erode the personal touch that residents value, and 80% fear staff resistance. Executives and property managers diverge sharply on where the risk lies: 96% of executives are concerned about the loss of the personal touch, compared to 71% of property managers, while property managers are less trusting of AI outputs than their leadership counterparts.

Advisory Council conversations are consistent with that pattern. Operators who have gone furthest in centralization tend to hold more nuanced views about its difficulty than those who have not yet begun, and the gap between executive intent and site-level execution is where implementations most commonly stall.

The tension between the workforce and residents is real and underreported. Among operators that have aggressively centralized, the most consistent finding has been that labor savings are smaller than projected, and the impact on resident satisfaction is greater than anticipated. BH Management, which manages more than 350 properties across 37 states, encountered this directly when it launched its first centralized support team in 2021, a renewal specialist program built on a platform separate from its existing CRM. Resident adoption was low, communication with prospective renewers stalled, and the program was eventually scrapped. The lesson, articulated by Melody King, BH’s COO of property operations, was that centralization surfaces operational inconsistencies that on-site teams had been quietly absorbing. “In managed multifamily, you expect that all of your teams are doing things the way that you have outlined,” King said, “and when you centralize, you realize that’s not the case.” The process of moving from 350 separate trained teams to a smaller set of portfolio-wide specialists involves a transition period that performance expectations rarely account for.

A framework for tiered centralization

The most enduring lesson from operators who have successfully navigated centralization is that the decision is not binary. The productive question is not whether to centralize, but which functions to centralize, to what degree, and for which asset types. Advisory Council discussions have surfaced a consistent framework built around three tiers:

Tier 1: High-volume, low-judgment transactions. This tier encompasses functions in which the interaction is largely transactional, the resident or prospect outcome is predictable, and human judgment adds marginal value compared with consistency and speed. Rent collection, maintenance request intake, application processing, and availability inquiries all fit this profile. These functions perform well in centralized models because errors are recoverable, residents have relatively low emotional investment in the interaction, and volume efficiency creates genuine cost leverage.

Advisory Council conversations consistently point to this tier as the strongest starting point for centralization across portfolio types and asset classes, and it is the category most amenable to AI-assisted handling without meaningful degradation of the resident experience. Initial renewal outreach can also fall within this tier, though the conversation shifts to Tier 2 once a resident’s specific circumstances or pricing objections come into play.

Tier 2: Context-dependent, moderate-judgment interactions. This tier includes initial conversations with prospective residents, follow-up on self-guided tour visits, application status communications, and coordination of non-emergency maintenance. These interactions benefit from the consistency and coverage advantages of centralization but require human judgment at identifiable moments. These moments include when a prospect’s question indicates a specific objection that can be addressed, when a maintenance request reveals an underlying issue that requires escalation, or when a renewal conversation touches on a resident’s specific circumstances.

Operators who have succeeded at centralizing this tier have done so by investing heavily in handoff protocols: the moment at which a centralized system transfers a prospect or resident to a human agent, and the quality of context that agent receives. Asset Living’s approach illustrates one version of a thoughtful Tier 2 architecture. The company has deployed virtual leasing concierges — centralized specialists each assigned to ten properties — whose role, as described by Pauline Houchins, Asset Living’s division president, is to function like “a fisherman capturing all the initial applications and inquiries that come in through in-person or chat service.” The concierges also set appointments for leasing agents and expedite the application process, with the flexibility to work on a site-specific basis when the property’s needs require it.

Tier 3: Relationship-intensive, high-judgment interactions. This tier covers move-in orientation, conflict resolution, escalated maintenance situations, community programming, and relationship management for long-tenure residents. Advisory Council operators are nearly uniform in their view that Tier 3 functions require an on-site or regionally proximate human presence.

AvalonBay’s neighborhood model, described by Michael Coyne, the company’s vice president of operations, represents one of the more developed attempts to extend the range of on-site presence while still achieving scale. In Coyne’s framing, the neighborhood is an evolution beyond the earlier pod model: rather than sharing a manager across two or three communities, the neighborhood groups up to five communities or up to 1,500 units under a shared team that distributes specialized work across the cluster. The whole team shares work, not just management. Advisory Council discussions are consistent with the view that this kind of regional proximity model preserves the high-judgment, relationship-intensive capacity that full centralization eliminates, while still capturing efficiency gains at the portfolio level.

The tiered framework does not produce a single operating model. It produces a decision architecture. A stabilized suburban garden community with a homogeneous resident base and predictable operational patterns can centralize more of Tier 2 than a Class A urban lease-up, where conversion rates are higher-stakes and on-site leasing expertise drives meaningful revenue outcomes. Centralization is not binary, and the competitive advantage comes from finding the optimal blend for each portfolio segment rather than applying a uniform model.

Advisory Council conversations reinforce the same point. Operators who have applied a single centralization strategy uniformly across a diverse portfolio consistently report that the model outperforms in asset types where Tier 1 and Tier 2 functions dominate, and underperforms in segments where Tier 3 presence is structurally more important to resident experience and lease conversion. The framework’s value lies in making those distinctions explicit before committing to a centralization architecture, rather than discovering them through underperformance after the fact.

Where the model gets complicated

Even operators with well-designed centralization frameworks encounter friction points that the framework alone does not resolve:

Career path disruption requires proactive management. The traditional multifamily leasing career path from leasing agent to leasing director to assistant manager to community manager depends on having distinct, learnable roles at the property level. Centralization removes or transforms several of those steps. The adjustment period for site managers who have long operated under conventional models is real, and the risk that the transition feels like a loss rather than an evolution is not trivial. Operators who have navigated this successfully have invested in clear, consistent communication about how roles evolve rather than disappear, framing centralization as a tool that removes routine work, allowing on-site staff to focus on the higher-judgment functions that define the resident experience.

Technology adoption is not automatic. The NAA research report sponsored by MRI Software found that 22% of operators plan to invest in upgraded technology platforms as part of their centralization strategy, and 21% are actively working to improve communication between centralized and on-site teams. Both priorities are correct, and neither is sufficient on its own. Platform investments that outpace training produce misuse, underutilization, and operational workarounds that recreate the inconsistency centralization was designed to eliminate. Advisory Council members who have overseen large-scale platform transitions consistently note that the time required to build genuine competency across a centralized team is substantially longer than initial rollout timelines suggest.

Resident perception of centralization is an active risk. Residents who encounter centralized operations without understanding why the model exists, or who encounter friction at moments they expected human support, tend to attribute the gap to cost-cutting rather than service improvement. Advisory Council conversations are consistent with the view that a centralized model without a clear escalation path to human support creates compounding dissatisfaction. The resident encounters a problem, cannot reach on-site staff, navigates a self-service channel not built for escalation, and attributes the entire experience to the operator’s indifference rather than a gap in the centralization design.

Implementation: Where to start

Centralization decisions made without a clear operational baseline tend to produce uneven results. Functions that could be centralized remain on-site by default, while resident-facing interactions get disrupted before back-office infrastructure is ready to support them. The five steps below offer a sequenced approach to implementation that Advisory Council operators have validated through direct experience.

1. Audit task volume and judgment intensity across the portfolio. Before making centralization decisions, operators should build a working inventory of what their on-site teams actually do and how often they do it. Advisory Council conversations consistently suggest that operators are surprised to find that a significant share of daily on-site activity consists of functions that fall cleanly into Tier 1, and that centralizing those functions alone frees meaningful on-site capacity without touching resident-facing interactions. Building a baseline operational inventory before committing to a centralized architecture makes the subsequent transition from dispersed site-level execution to a portfolio-wide specialist model credible to both ownership and on-site staff.

2. Pilot centralization on billing and collections before leasing. Michael Coyne, AvalonBay’s vice president of operations, recommends beginning with back-office functions before extending centralization to resident-facing operations. “Start with a pilot program, preferably something less complex like billing,” Coyne has said, “and let user feedback and operational metrics guide your expansion.” The reasoning behind that sequencing, consistent with Advisory Council discussions, is that billing centralization produces measurable efficiency gains with limited resident exposure to the centralized model, builds organizational confidence in the approach, and establishes the operational infrastructure required for more complex centralization later. Operators who establish the back-office foundation first tend to encounter fewer conversion and satisfaction gaps than those in more aggressive centralization rollouts.

3. Invest in designing handoff protocols before scaling Tier 2 centralization. The quality of the transition from a centralized system to a human agent is among the most operationally significant design decisions in remote leasing. Operators should be able to articulate specifically what context the human agent receives at the moment of handoff, how long the transfer takes, and what the prospect experiences during that interval. Advisory Council members who have examined conversion data consistently identify handoff friction as the primary driver of conversion losses in centralized leasing models, rather than self-guided tour mechanics or AI response quality. The pattern is recognizable across portfolio types: the centralized first-touch performs well, the on-site team performs well, and the gap between them is where prospects disengage.

4. Differentiate the model by asset class and resident profile. A single centralization strategy applied uniformly across a diverse portfolio will produce uneven results that are difficult to diagnose. Operators should treat Class A urban lease-ups, stabilized suburban communities, affordable housing properties, and senior communities as distinct operational contexts with different centralization thresholds at each tier. Operators who have applied uniform centralization strategies across diverse portfolios consistently report that the model outperforms in asset types where Tier 1 and Tier 2 functions dominate, and underperforms in segments where Tier 3 presence is structurally more important to resident experience and lease conversion.

5. For third-party managers, sequence PMA amendments strategically. Operators in the third-party context should identify properties where the ownership relationship supports centralization, pilot the model there first, and rigorously document performance outcomes before approaching other ownership groups. The 20for20 research makes clear that leading third-party managers are finding paths through the PMA amendment constraint, not by solving it at the portfolio level, but by building enough demonstrated performance data to make the case, property by property. Advisory Council conversations are consistent with that sequencing: institutional partners with sophisticated asset management teams and strong alignment on operational strategy tend to be the most productive starting points for pilots, both because they are more likely to approve PMA amendments and because they are better positioned to evaluate and act on the performance data that results.

The constraint was never the tooling

Centralization is not a single decision. It is a series of calibrated choices about which functions to move, to what degree, on which timeline, and for which asset types. Operators who treat it as a binary will find that the model underperforms in segments where on-site judgment matters most, and that the cost savings in other segments are insufficient to offset losses in resident experience and conversion.

The technology to support sophisticated centralization exists and is continuing to mature. AI-assisted maintenance triage, virtual leasing concierges, portfolio-wide performance intelligence platforms, and integrated capital planning tools are all delivering measurable results for operators that have implemented them with the requisite organizational design. The constraint is not tooling. Operators who invest now in building the organizational infrastructure will hold a meaningful advantage in efficiency and NOI over those who delay. The conversation around centralization is shifting from proof of concept to competitive differentiation, and the window for first-mover advantage is closing.

– Nick Pipitone