Multifamily operators are entering the second half of 2026 with a familiar set of pressures coming from both sides. Rent growth has softened significantly from its post-pandemic peak, yet the cost side of the ledger, including labor, insurance, materials, and contracted services, has not followed suit.

The result is a margin environment in which revenue-side solutions are largely unavailable, and the operators who outperform will be the ones who have turned controllable operating expenses into a management discipline rather than a residual of site-level discretion.

Procurement is the category where that discipline is both most achievable and most frequently neglected. Across a typical mid-sized portfolio, vendor relationships are managed property by property and spend data lives in PMS exports that no one has standardized or consistently monitored.

This report, drawn from Blueprint Advisory Council discussions with operators managing portfolios ranging from a few thousand to more than 50,000 units, maps the procurement maturity framework those conversations have surfaced: the three layers operators should build, the tensions that complicate implementation in practice, and the five steps that translate the framework into measurable savings.

Three forces making procurement urgent

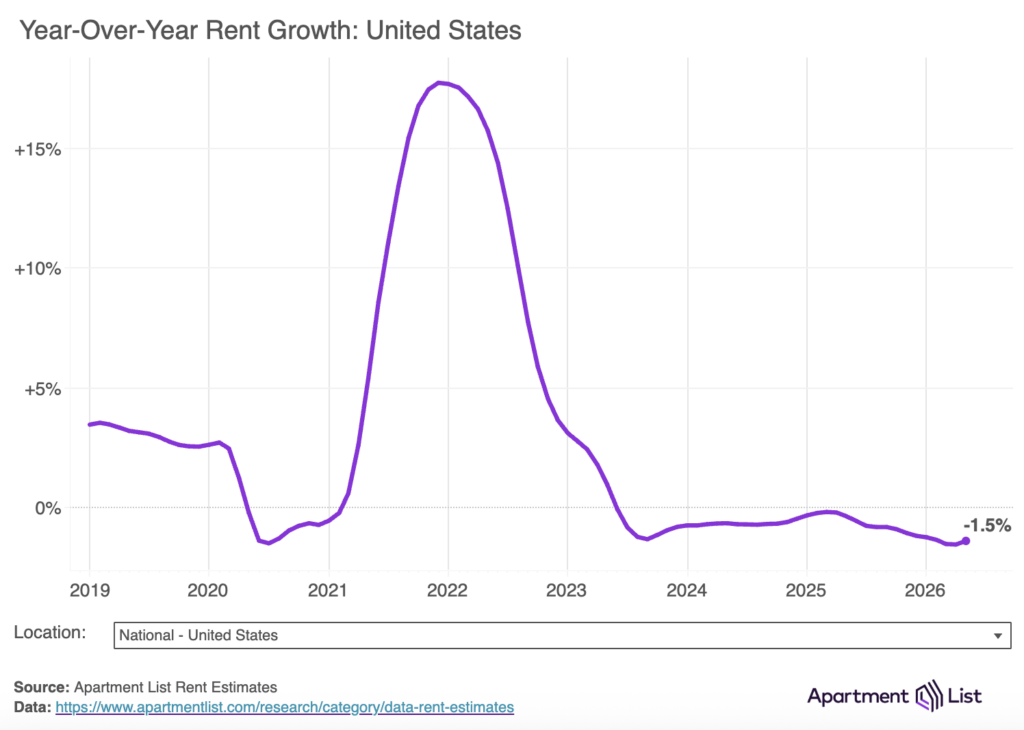

The margin compression cycle. The national median monthly rent stands at $1,379, down 4.4% from its mid-2022 peak, according to Apartment List’s June 2026 National Rent Report. The gradual decline has continued for roughly three years, driven largely by a historic surge in multifamily supply rather than any meaningful softening in demand. Even so, median rents remain 20% above their early-2021 baseline.

But as rent growth has softened, labor costs, insurance premiums, and material prices have all increased meaningfully over the past three years. That combination puts controllable operating expenses — the category procurement directly affects — under more scrutiny. Blueprint Advisory Council conversations consistently surface the same observation: operators who cannot grow revenue have no choice but to systematize cost.

The consolidation dynamic. Capital concentration in alternative investments is accelerating. The top five fundraisers in the retail alternatives space — Blackstone, KKR, Cliffwater, Ares, and Blue Owl — collectively raised roughly $92 billion in 2025, representing approximately 45% of total industry inflows, according to Stanger. The gap between operators with centralized procurement and those without is becoming a cost disadvantage rather than a management style difference. Large operators are already acting on this: firms like Cortland are investing in centralized procurement, consolidating vendor relationships, leveraging group purchasing power, and insourcing services such as pest control and valet trash to drive cost out of the system.

A 50,000-unit operator negotiating national supply contracts through a GPO relationship operates with a different cost basis than a 5,000-unit operator managing vendor relationships property-by-property. GPOs create leverage through combined member spend, motivating suppliers to offer pricing and contract terms that individual members couldn’t achieve on their own. In a market where revenue growth is constrained, the cost-basis gap increasingly determines which operators can underwrite acquisitions competitively and which cannot.

The owner expectations shift. Institutional ownership groups are raising documentation requirements across the board. Three competitive bids, consistent vendor qualification records, and exportable audit trails are becoming standard requirements in asset management agreements. Advisory Council operators report that ownership group requests for procurement documentation have increased substantially over the past 18 months, driven by both lender requirements and LP-level ESG and governance standards. Manual procurement processes are increasingly incompatible with the documentation requirements attached to institutional capital.

The procurement maturity framework

Advisory Council conversations point to a clear pattern: the operators capturing the most savings aren’t just buying better software. They’re treating procurement as a discipline built in stages. They start with compliance, move to spend visibility, and eventually reach strategic sourcing. The framework has three layers, and the sequence matters:

Layer 1: Compliance-first vendor qualification. The entry point of any scalable procurement function is a controlled vendor pool. Before price negotiation, contract standardization, and spend analytics, operators need to know that every vendor entering their portfolio carries the correct insurance, holds the required licenses, and meets the documentation standards required by their ownership agreements.

Platforms like NetVendor, which maintain a pool of nearly 100,000 pre-vetted vendors, address this by automating COI collection, credential verification, and renewal tracking. When vendors are pre-qualified before a bid event, sourcing cycles compress significantly because the compliance step is already complete. Operators in the Advisory Council who have moved to compliance-first frameworks report that project timelines improve, not because bids move faster but because the back-and-forth on missing certificates disappears.

Layer 2: Centralized spend visibility. The second layer is the one most operators attempt to shortcut, and the shortcut reliably fails. Spend visibility requires clean, categorized data. Not the raw output of a PMS export, but transaction data that has been reconciled, categorized by service type, and attributed to vendor relationships rather than individual invoices. Advisory Council operators who have implemented AI-assisted spend analytics consistently describe the same discovery experience: spend concentration is almost never where they expected it, and consolidation opportunities are hiding in categories that seemed too small to matter.

A portfolio that discovers it has 14 different landscaping vendors across a single market — each negotiated independently by site teams — is seeing a consolidation opportunity worth tens of thousands of dollars annually that was invisible without structured spend data. Platforms like RealPage’s Source to Pay suite and OMNIA Partners’ Spend Path tool are specifically designed to surface these patterns at portfolio scale.

Layer 3: Strategic sourcing and contract standardization. The third layer is where the largest operators are operating and where the margin impact is most visible. Strategic sourcing means approaching major spend categories as portfolio-level contracts rather than property-level relationships. Cortland, for example, has moved toward integrated facilities management that consolidates vendor relationships and leverages group purchasing power, while simultaneously insourcing categories such as pest control and valet trash.

Cardinal Group, managing over 50,000 units, engaged OMNIA Partners to centralize its purchasing strategy and identified significant savings by eliminating rogue spending and renegotiating consolidated contracts. The structural move at this layer is shifting from per-property vendor relationships to per-market or per-region master service agreements with two to three vetted providers.

Where the framework gets complicated

The procurement maturity framework is straightforward in structure. Implementation is harder, and Advisory Council conversations identify three tensions that determine whether operators actually capture the savings the framework promises.

Centralization versus local market variability. National and regional contracts deliver pricing consistency, but multifamily operations are local. A landscaping contract that works well across Sunbelt suburban assets may not translate to urban high-rise properties in the same portfolio. Operators who have pushed too hard toward national standardization report vendor performance degradation in markets where local providers were genuinely superior. The resolution most Advisory Council operators have arrived at is a hybrid model: national contracts for commodity purchases and major non-site-specific services, with local market consolidation for services where geographic specialization matters. This model captures most of the pricing benefit while preserving enough flexibility to match vendor capabilities to asset type.

PMS fragmentation. Large portfolios rarely run on a single property management system. Operators managing assets across Yardi, RealPage, Entrata, and MRI simultaneously face a data synchronization problem that undermines spend visibility before it starts. Manual reconciliation across PMS platforms introduces the same errors and delays that centralized procurement is designed to eliminate.

The implication is that procurement technology investments need to be evaluated for deep PMS integration capability, not just for their standalone feature set. A spend analytics tool that cannot ingest clean data from all operating systems in a portfolio will produce insights that cover only a portion of actual spend. That partial visibility can be worse than no visibility if it leads to false confidence in where consolidation has been achieved.

Cultural resistance at the site level. The operational logic of centralized procurement is clear at the portfolio level. It is less obvious, and often actively resisted, at the property level. Site teams that have managed vendor relationships independently for years experience procurement standardization as a loss of autonomy rather than an operational improvement. The operators who have navigated this transition most successfully have done two things. First, they demonstrated quick wins through measurable cost reductions within 90 days of implementation. Second, they built site-team input into the vendor qualification process so that property-level knowledge of vendor performance informs the approved vendor list rather than being overridden by it.

5 steps to implementation

Audit current spend by category and vendor. Before any tech purchase or vendor consolidation initiative, operators need a complete picture of what is actually being spent, on what, and with whom. This means pulling transaction data from all operating systems, normalizing it against a consistent category taxonomy, and identifying concentration by vendor, market, and asset type. Most portfolios discover that 20% of their vendors account for 80% of spend, and that the tail of long vendors includes dozens of relationships that could be consolidated without any service degradation.

Establish a compliance-first vendor onboarding standard. Define the minimum compliance requirements for each vendor category and implement a systematic process to verify and renew those credentials. This step is foundational because it determines which vendors are eligible to participate in future bid events. Operators who attempt to run competitive sourcing without a pre-qualified vendor pool find bid quality inconsistent, and compliance issues surfacing after work has already been awarded.

Consolidate the largest spend categories at the market level. Rather than attempting portfolio-wide consolidation immediately, start with the three to five largest recurring service categories in the highest-concentration markets. Landscaping, pest control, and waste management are typically the best starting points because they are high-frequency, well-defined in scope, and readily comparable across vendor proposals. Issuing standardized RFPs to pre-qualified vendors in these categories, with side-by-side bid comparison, typically yields 10–20% cost reductions in the first cycle.

Select procurement technology with PMS integration as a primary criterion. Procurement platforms are only as useful as the data flowing into them. When evaluating technology, prioritize vendors with proven integration to the PMS platforms in the portfolio, not just the most feature-rich standalone tools. The ability to automatically pull clean transaction data, match it to vendor records, and produce categorized spend reports without manual reconciliation determines whether spend visibility is operational or theoretical.

Build the governance layer: policy, training, and accountability. Centralized procurement requires a policy framework that site teams understand and follow. This means documented approved vendor lists, clear purchase authorization thresholds, defined escalation paths for exceptions, and regular spend reviews that surface off-contract purchasing before it becomes a pattern. Advisory Council operators who have sustained procurement savings over multiple years attribute that durability not to technology but to governance and the consistent reinforcement of procurement standards through performance management and data visibility.

The foundation matters now

The operators who will outperform on NOI through the remainder of this cycle are not the ones with the most sophisticated procurement technology stack. They are the ones who have built procurement into their operating model as a management discipline, with standardized vendor qualification, centralized spend visibility, and contract structures that capture portfolio-scale leverage.

The procurement maturity framework outlined in this report is an organizational capability enabled by technology. The compliance layer prevents vendor risk from entering the portfolio at the point of entry. The spend visibility layer turns transaction data into consolidation intelligence. The strategic sourcing layer converts that intelligence into negotiating leverage. Each layer builds on the previous one, and operators who attempt to skip to strategic sourcing without the compliance and visibility foundations typically find that savings are temporary because the governance infrastructure is not in place to sustain them.

The consolidation trend in institutional multifamily ownership creates a direct link between procurement capability and portfolio competitiveness. As larger operators build procurement strategies that deliver significant cost advantages, mid-sized operators face a choice. They can build that capability now or accept a permanent cost disadvantage that compounds with every acquisition. The operators who make that investment in the current compressed-margin environment will be positioned to generate better returns meaningfully when the rent growth cycle turns.

– Nick Pipitone